TLDR

In the RWA sector, the first explosion is from fixed-income products, driven by the treasury management demands of DAOs and Web3 companies. The top TVL rankings in the RWA sector are dominated by tokenized U.S. Treasury Bill projects.

By incorporating RWA, DAOs can retain high liquidity for their assets while generating stable income with low correlation to on-chain activities, thus achieving better quality returns and risk diversification.

The governance and operations of DAOs are not necessarily more efficient than traditional corporate structures. MakerDAO incurs high costs to purchase U.S. Treasury Bill ETFs through a complex trust structure, which is not feasible for most other DAOs and Web3 companies.

In comparison, it is more efficient and feasible for DAOs to purchase tokenized RWAs on-chain through professional/compliant asset issuers.

RWA coming into mainstream crypto

Against the backdrop of the crypto winter and rising US interest rates, the new wave of DeFi innovation has not yet arrived. Native DeFi protocols are experiencing a sharp decline in yields, with stable yield rates even lower than U.S. Treasury bonds, the so-called "risk-free rate." Many DeFi projects are shifting their focus beyond the crypto world to real-world assets (RWA). Among the mainstream DeFi protocols, MakerDAO was one of the earliest to venture into RWA. As early as 2020, MakerDAO collaborated with 6s Capital, a real estate development collateralized loan project, to establish an RWA vault. Subsequently, in partnership with Centrifuge, a lending platform based on RWA, Centrifuge tokenized off-chain assets. MakerDAO purchased these tokens as collateral to generate the stablecoin Dai, diversifying the collateral for Dai. MakerDAO's Endgame Plan, released in May 2022 by MakerDAO cofounder Rune Christensen, also includes using RWA as collateral to build a decentralized stablecoin system.

In recent times, major DeFi protocols have made various moves in the RWA space. In June 2023, Robert Leshner, the founder of Compound, established a new company called Superstate and filed documents with the SEC, aiming to create a short-term U.S. Treasury bond fund on the Ethereum platform. MakerDAO's new MIP65 (MakerDAO improvement proposal, “MIP”) proposal, which involves deploying a portion of MakerDAO funds to invest in short-term bond Exchange-Traded Funds (ETFs), passed in May 2023. The proposal increased the vault's debt ceiling from $500 million to $1.25 billion, with plans to purchase the corresponding amount of bond ETFs in the coming months. Furthermore, prominent financial giants, including Goldman Sachs and Citigroup, have expressed their interest in this field and even entered the competition.

Why now?

In fact, there was a wave of STO (Security Token Offering, which is also one part of RWA) hype in 2018. However, the hype from that year fizzled out. Now, similar topics are being discussed again, but why at this particular time? What are the driving forces behind this development?

- From an infrastructure perspective, the DeFi infrastructure has gradually improved, with well-established token standards, oracles, and peripheral development tools that can bridge the gap between on-chain and off-chain.

- From an asset and yield perspective, Web3-native assets have reached a bottleneck, with assets becoming relatively homogeneous. In a bear market scenario, on-chain activities have been sluggish, and there is a lack of native stable sources of yield.

- From a narrative perspective, after the collapse of CeFi, there is a heightened focus on compliance and risk management. The traditional financial sector has always been highly regulated, and RWA assets provide better investor protection compared to other crypto-native assets.

- From a legal and regulatory perspective, regulators are also learning and progressing, leading to the improvement of legal and regulatory frameworks related to cryptocurrencies.

In the previous market cycle, similar RWA platforms also made initial developments. These platforms operated by utilizing community governance to provide lending pools for institutions. Users could invest in these pools to earn pre-determined yields, while institutions could utilize the funds for related investment activities and repay the interest and principal as agreed upon. Examples of such platforms include Maple Finance, Clearpool, and TrueFi. However, with the collapses of Luna and FTX, several related institutions went bankrupt. The early RWA platforms lacked compliance processes and risk management. Some borrowers defaulted, leading to the inability to repay the borrowed assets, resulting in significant losses for investors. Developers have learned from these experiences to avoid similar pitfalls in the future.

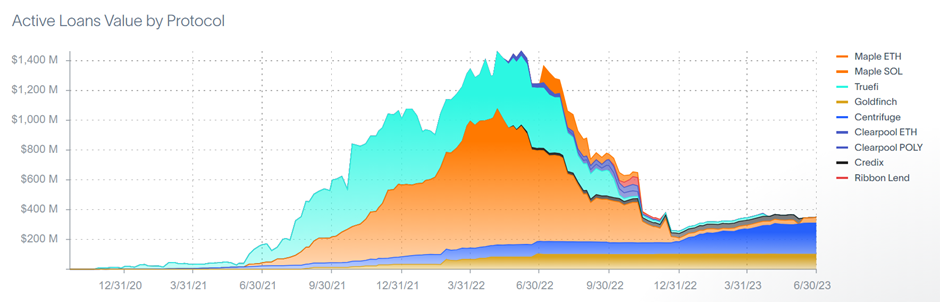

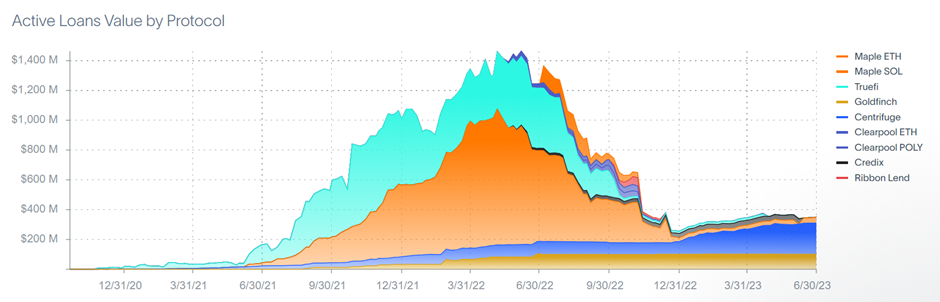

Figure 1: RWA active loans value by protocol, Source: RWA.xyz, data as of 2023.07.06

As seen in the chart above, at the time of the Luna collapse in mid-2022, the active loan volume reached its peak and then sharply declined. One of the most significant events occurred was the TPS Capital lending pool opened on Clearpool.

TPS Capital was partnered with Clearpool Finance as a borrower pool in Q2 of 2022. During their partnership, TPS Capital had a complicated corporate structure that obscured its relationship with Three Arrows Capital, leading to claims of independence from the latter.

With Luna’s collapse, Three Arrows Capital went bankrupt. However, court filings prepared by Three Arrows’ liquidators showed the two were tightly connected, with Three Arrows acting as a guarantor for TPS for loans on which it later defaulted.

In June 2022, Clearpool removed TPS Capital from its lending pool, and Clearpool's data partner, X-Margin, downgraded TPS Capital's rating to B, reducing the lending limit to $0. Clearpool and X-Margin announced that they would work together to ensure the repayment of TPS Capital's borrowed funds, safeguarding users from losses.

Those millions of losses are lessons learned for RWA developers, and now they realized to focus more on compliance and legal structure while building RWA.

What is a Real-World Asset (“RWA”)

RWA refers to various assets that exist outside the blockchain but can be tokenized and integrated with existing DeFi protocols through certain methods. Currently, the main types of RWA projects are focused on the following categories:

- Bonds, including private bonds, corporate bonds, and government bonds.

- Real estate.

- Equities.

- High-value collectibles.

- Carbon credit scores.

We believe that the earliest RWA products to enter DeFi will be bond-based products, including government bonds and corporate bond products. The demand side is primarily driven by the adoption of RWA by DeFi protocols and Web3 protocol treasury management. Currently, according to data from DefiLlama, the top two RWA platforms in terms of Total Value Locked (TVL) are tokenized U.S. Treasury Bill platforms (OpenEden and MatrixDock), followed by real estate related RWA platforms (Tangible and RealT). However, the overall size of the RWA market, with a few hundred million dollars in total value, is still very small compared to both DeFi and the traditional financial industry, indicating significant room for growth.

Figure 2: RWA TVL rankings, Source: DefiLlama, data as of 2023.07.10

The driving force behind RWA

Generally, existing DeFi protocols have three ways to integrate RWA assets:

1. Treasury management: Some RWA demand for MakerDAO, for example, comes from treasury management.

2. Collateralization: RWA assets can be used as collateral in protocols. Some examples are MakerDAO and UXD protocol (a stablecoin protocol in the Solana ecosystem, bought $5M U.S. Treasury Bill token from OpenEden as collateral for its USD stablecoin)

3. Introducing new asset types for DeFi scenarios: DeFi protocols integrated with those assets, such as Curve (allow MatrixDock’s STBT to trade) and Flux Finance (enable lending for Ondo Finance’s OUSG).

Why do DeFi protocols need RWA? There are multiple motivations for introducing RWA, including:

- On-chain asset management demand: On-chain asset management seeks stable returns and better liquidity. RWAs such as government bonds are widely recognized as investment targets with good liquidity and low risk.

- Alternative yield source: Native on-chain yields primarily come from staking, trading, and lending activities. However, the volatile nature of the crypto market can lead to decreased yields during market downturns, as we are currently experiencing. Mainstream platforms are now offering stablecoin yields that are even lower than U.S. government bonds. Introducing RWA-related assets can provide relatively higher yields that are less correlated with on-chain activities.

- Portfolio diversification: Investing solely in crypto-native assets can lead to a highly concentrated and volatile portfolio. By introducing stable RWA assets that are less correlated with native on-chain assets, investors can achieve diversification and build a more robust and effective investment portfolio.

- Introducing diversified collateral: The high correlation among crypto-native assets can result in potential runs on lending protocols or large-scale liquidations, exacerbating market volatility. Introducing RWA assets that have a lower correlation with on-chain crypto-native assets can effectively mitigate such issues.

Let's take MakerDAO as an example to analyze how DeFi protocols adopt RWA.

MakerDAO’s RWA layouts

MakerDAO is a decentralized autonomous organization (DAO) that aims to create and manage the Ethereum-based stablecoin Dai. Users lock Ethereum (ETH) as collateral to generate Dai stablecoins. The current goal of Dai is to maintain a 1:1 peg to the US dollar, stabilizing its value through smart contracts and algorithms, then it will try to build a decentralized stable currency according to MakerDAO’s Endgame Plan. Due to the high volatility of the cryptocurrency market, relying on a single collateral asset can lead to significant liquidations. Therefore, MakerDAO has been actively exploring ways to diversify its collateral, and RWA is an important component, even being mentioned in the Endgame Plan proposed by MakerDAO Cofounder Rune Christensen.

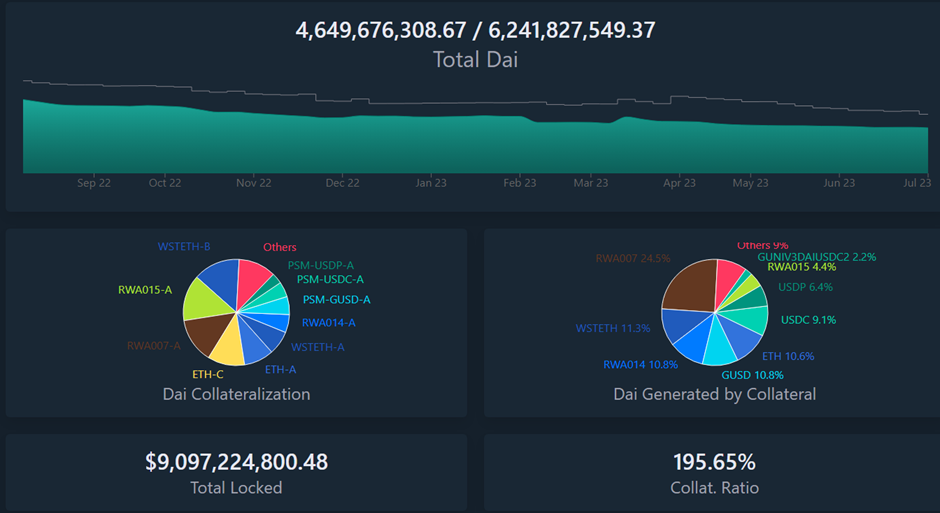

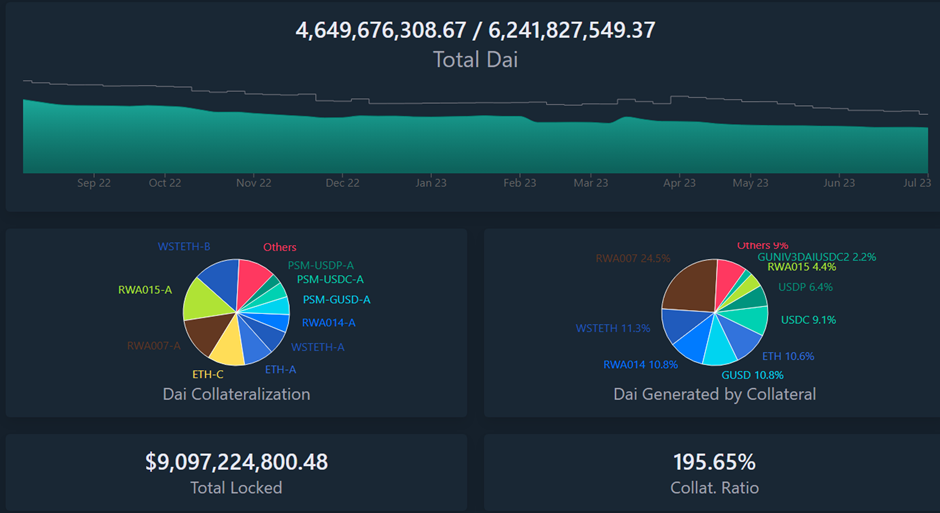

Figure 3: Current Dai stats, Source: daistats.com, data as of 2023.07.10

From the figure above, the current total supply of Dai is approximately 4.6 billion. MakerDAO has set a total supply cap of 6.2 billion Dai. Currently, the collateral backing Dai has become more diversified, including a portion of RWA and various other stablecoins.

Aftermath of single collaterals

On March 12, 2020, the crypto market experienced a market collapse. On one hand, due to limited Ethereum network performance and Ethereum network congestion, the Liquidation Module powered by the Maker system functioned inadequately, leading to a low level of engagement of liquidators; on the other hand, the market price plunge of various crypto assets caused Vault owners to repay Dai debt and close their Vaults, coupled with the increasing market demand for Dai, resulting in Dai liquidity on the verge of depletion. The above two reasons led to a substantial amount of bad debt of up to 5.67 million Dai surfacing in the MakerDAO system, resulting in the first Debt Auction taking place in MakerDAO since its inception. MakerDAO commenced a total of 106 Debt Auctions, which lasted from March 19 to March 28, 2020, raising a total of 5.3 million Dai with 20,980 MKR.

MakerDAO’s Endgame

After experiencing such events, MakerDAO has continuously attempted to diversify its collateral. However, it is inherent that native crypto assets have a high degree of correlation. The goal of the MakerDAO system is to gradually establish a decentralized stablecoin and to build a monetary system. To achieve this, it needs to use currently accepted assets as collateral and leverage their credibility. Native cryptocurrencies naturally play an important role as collateral. Additionally, to diversify the risks in the current crypto market, MakerDAO has introduced some RWA assets as collateral for the stablecoin Dai.

The Endgame Plan is a series of future visions and plans for MakerDAO proposed by Rune Christensen, the co-founder of MakerDAO, in May 2022. It outlines the path for building a decentralized stablecoin. This ultimately requires two types of collateral: decentralized assets that can ensure fairness on a physical level, and RWAs that can provide reliable liquidity and stability. Furthermore, specific impacts need to be created to demonstrate the benefits that DeFi, Maker, and the Dai stablecoin can bring to the world, gradually integrating the world's economic system with DeFi and adopting Dai as a tool for payment and settlement.

Endgame has three phases, and each phase is called stance, with each stance categorized based on the composition of collateral, aiming to ultimately establish Dai as a decentralized stable currency:

- Pigeon stance (Current stance): no ceiling for RWA as collaterals, and stablecoin Dai stays pegged to the US dollar.

- Eagle stance: Dai will have a negative target interest rate and Dai might become unpegged from the dollar.

- Phoenix stance: The collateral for the stablecoin Dai no longer includes any other types of RWA besides physical resilience RWAs.

Specific ratios for the collateral in each phase were designed in the detailed plan. For specific details, please refer to the original text, as it is not further elaborated here.

Endgame Plan v3 complete overview - Legacy / Governance - The Maker Forum (makerdao.com)

Composition of MakerDAO’s RWA

Throughout the history of currency, we have seen the progression from early commodity money, where consensus was formed around scarce resources like shells and gold, to the issuance of paper money backed by collateralized scarce resources, and eventually to the issuance of credit-based currencies backed by military force. Although MakerDAO's Dai has a significant volume in the billions, it is still relatively small in the larger context. It needs to leverage the credit of other assets and demonstrate its strengths to gradually solidify its position. This is why RWA is introduced as an intermediate transitional state in the Endgame roadmap proposed by MakerDAO’s cofounder: in a crypto asset world that is not yet solid enough, real-world assets are needed as an anchor for building a stable currency.

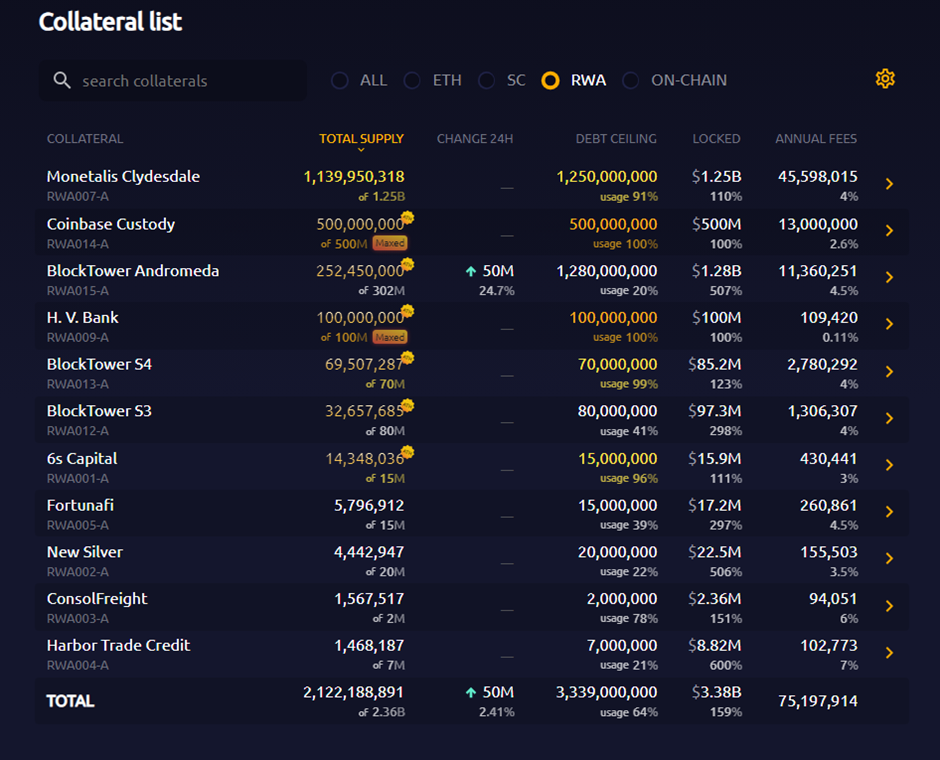

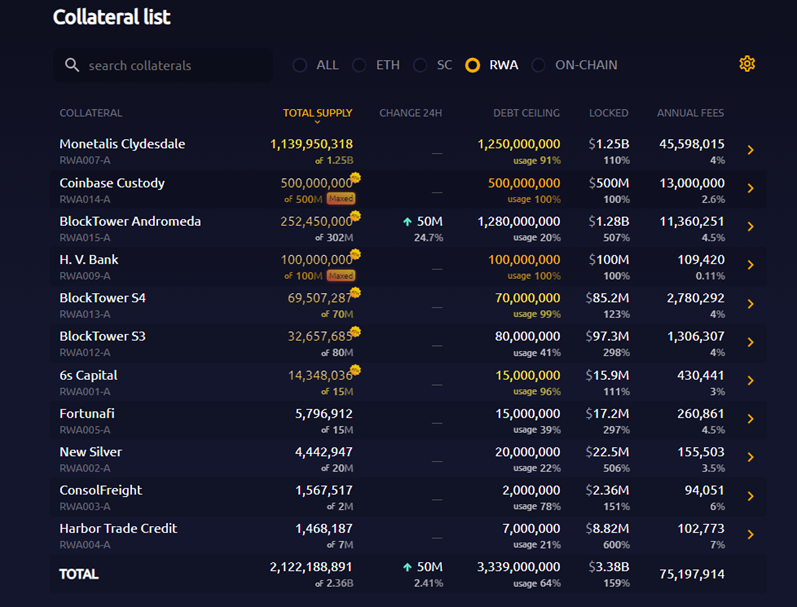

According to data from MakerBurn.com, there’s 11 RWA-related projects are used as MakerDAO’s collaterals, with 2.7 billion TVL.

Figure 5: MakerDAO RWA, Source: MakerBurn.com, data as of 2023.07.10

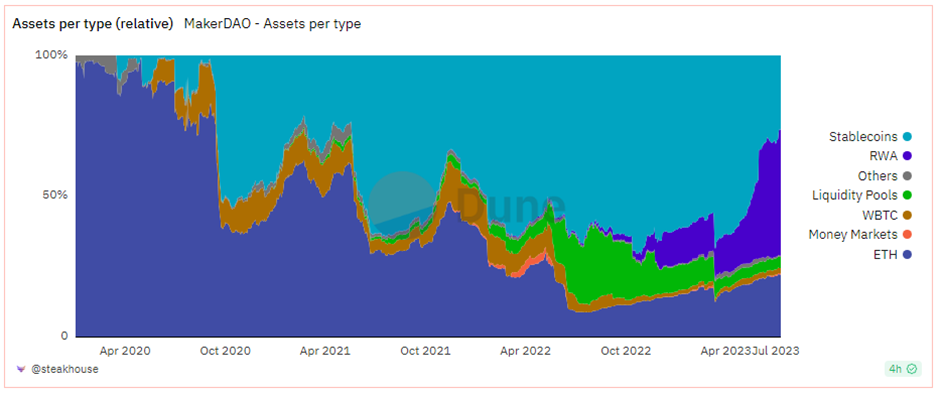

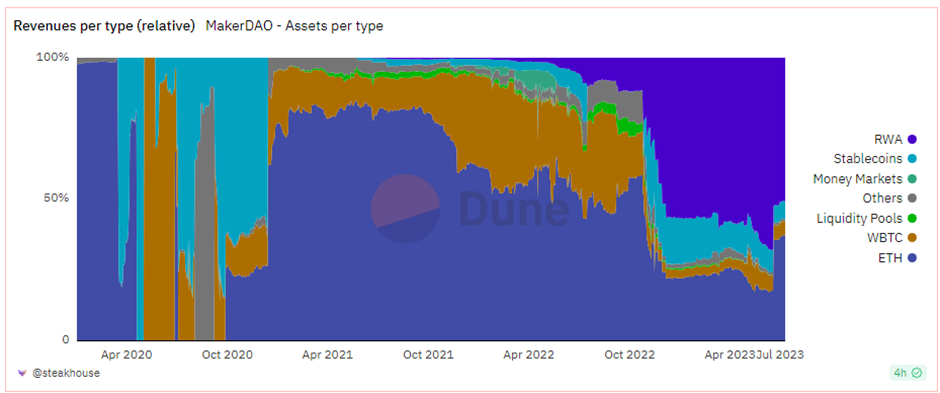

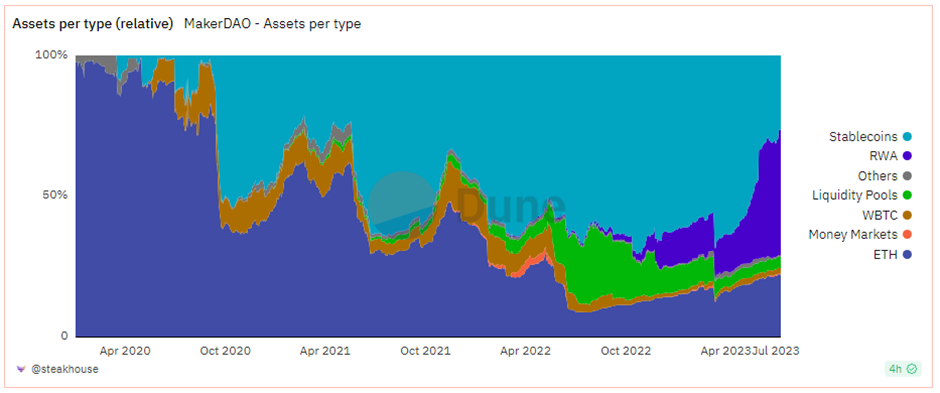

Figure 6: MakerDAO asset composition, Source: Dune.com, data as of 2023.07.10

The blue section in the middle on the right-hand side represents the proportion of RWA in MakerDAO’s treasury, which currently stands at 41.5%.

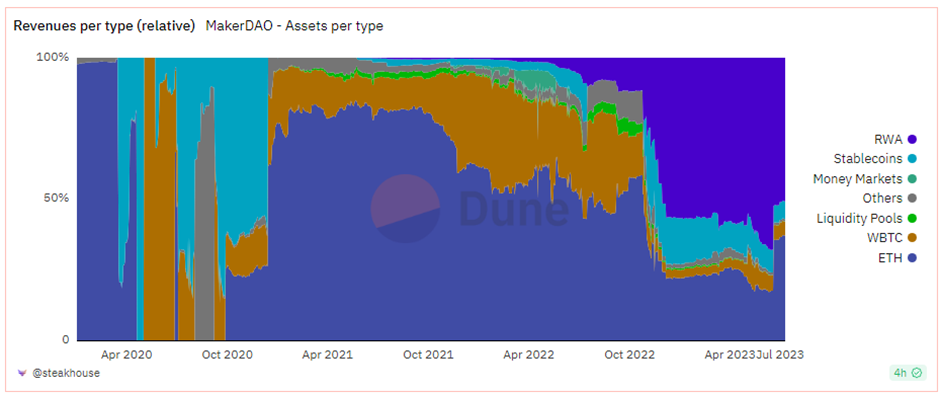

Figure 7: MakerDAO revenue, Source: Dune.com, data as of 2023.07.10

And the profit from RWA accounts for 51.1% as shown in the upper-right section.

In June 2023, through a proposal, MakerDAO increased the Dai Saving Rate (the risk-free rate for Dai) from 1% to 3.49%, providing attractive returns for Dai holders. The yield source comes from those RWAs.

MakerDAO's RWA mainly consists of four parts:

- RWA 001, 6s capital, providing real estate loans.

- MIP81, known as RWA014, proposed by Coinbase Institutional, which involves depositing a portion of MakerDAO's USDC into Coinbase USDC Institutional Rewards, offering a 1.5% APY based on USDC.

- Assets tokenized by the decentralized lending platform Centrifuge, with MakerDAO purchasing related tokens, including New Silver (real estate lending) and BlockTower (structured credit), among others.

- MIP65, known as Monetalis Clydesdale, proposed by Monetalis, which involves using MakerDAO's stablecoins to purchase short-term bond ETFs. The proposal was initially passed in October 2022 (with $500 million), and the debt ceiling was increased in May 2023 (to $1.25 billion).

Among these, 6s capital and Coinbase are separate partnership cases.

This research will focus on discussing Centrifuge and Monetalis Clydesdale to explore how DeFi protocols integrate with RWA. The related issues involve not only smart contracts and business models but also governance frameworks, legal frameworks, asset ownership, and more.

How can a DAO invest in U.S. Treasury Bill? MakerDAO’s Monetalis Clydesdale

MIP65, known as Monetalis Clydesdale, was proposed by Allan Pedersen, the founder of Monetalis, in January 2022. It was passed by the MakerDAO community and implemented in October 2022, with an initial debt ceiling of $500 million. In May 2023, a subsequent proposal increased the ceiling to $1.25 billion.

In the community discussion of MIP13, which was proposed in February 2022, it was noted that approximately 60% of MakerDAO's balance sheet consisted of various stablecoins (with the Peg Stability Module or PSM mechanism ensuring the stability of Dai's value, primarily backed by USDC). Over the past 18 months, more than 50% of the assets were stablecoins, but they did not generate profits for MakerDAO. The main counterparty risk was associated with Circle (the issuer of USDC). The community wanted to find ways to invest in stablecoins and generate profits while diversifying risk. One of the ideas proposed was to invest in short-term U.S. Treasury bonds.

In the final vote among the participants of the MIP65 proposal, 71.19% supported the proposal, and it was ultimately approved. MIP65 will establish an RWA-related vault, where funds from MakerDAO's PSM mechanism will be invested in high-liquidity bond strategies through a trust structure.

Monetalis is a consulting firm founded by Allan Pedersen and Alessio Marinelli. It provides consulting services and solutions to traditional finance and DeFi institutions. Both founders have extensive experience in traditional finance, consulting, and venture capital. Monetalis' investors include UDHC, Dragonfly, and Rune Christensen, the co-founder of MakerDAO.

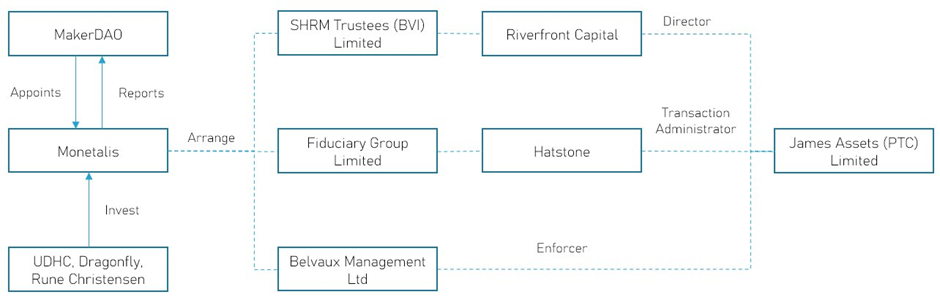

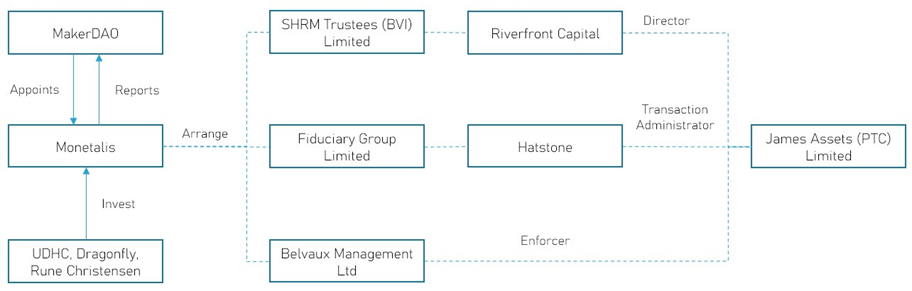

In the case of MakerDAO, Monetalis is the proposer and project manager. The overall business architecture of the proposal is as follows:

- MakerDAO delegates the design of the overall architecture to Monetalis through voting, and Monetalis is required to provide periodic reports to MakerDAO.

- Monetalis designs the overall structure of the trust, where:

- Riverfront Capital Ltd (SHRM Trustee (BVI) Limited) serves as the sole director.

- Hatstone (Fiduciary Group Limited) acts as the transaction administrator, responsible for monitoring and approving transactions within the trust.

- Belvaux Management Ltd serves as the trustee enforcer. It must monitor the activities of the Share Trustee to ensure that it is using the assets subject to the Share Trust in such a way that achieves or furthers its purpose(s) and that the Share Trustee is otherwise properly administering the Share Trust.

- Each holder of Dai and each holder of MKR is a beneficiary of the Trust. MKR token holders, by a resolution, will direct JAL to acquire and/or dispose of the ETFs.

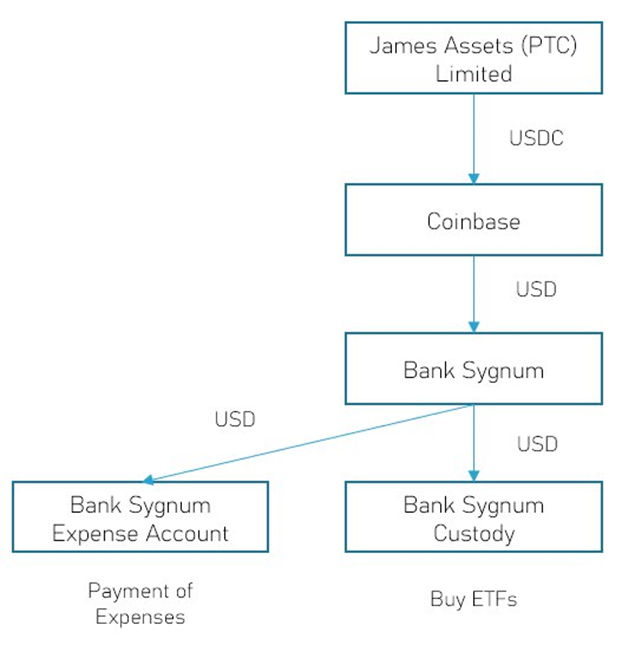

- James Asset (PTC) Limited, also known as JAL, is a simple shell company to hold trust. The company was created and the original shareholder was SHRM Trustees (BVI) Limited.

- Coinbase provides exchange services for USDC and USD.

- Sygnum Bank facilitates the trading and custody of trust assets, and a separate account is set up for the operational expenses of the trust.

The funds are invested in two types of ETF products: Blackrock's iShares US$ Treasury Bond 0-1 yr UCITS ETF and Blackrock's iShares US$ Treasury Bond 1-3 yr UCITS ETF.

Among those:

- JAL is a shell company that holds the trust and was newly established in the British Virgin Islands (BVI).

- SHRM Trustee (BVI) Limited is a company established in the 1990s that provides professional trust services.

- Hatstone (Fiduciary Group Limited) has over $1 billion in total assets and offers services such as fund management, corporate services, and investment funds.

- Monetalis, acting as the project manager under the delegation of MakerDAO, is responsible for establishing the overall architecture. The situation of Monetalis does not affect the assets of MakerDAO. Monetalis receives an annual management fee of 0.15%, paid quarterly.

- Sygnum Bank is the world's first regulated digital asset bank and a digital asset specialist with a global reach, headquartered in Switzerland and Singapore. Its products include regulated cryptocurrency trading. With Sygnum Bank AG's Swiss banking license and Sygnum Pte Ltd's capital markets services (CMS) license in Singapore, Sygnum empowers institutional and private qualified investors, corporates, banks, and other financial institutions to invest in the digital asset economy with complete trust.

Figure 8: Structure of the Trust, Source: DigiFT Research, MakerDAO MIP65

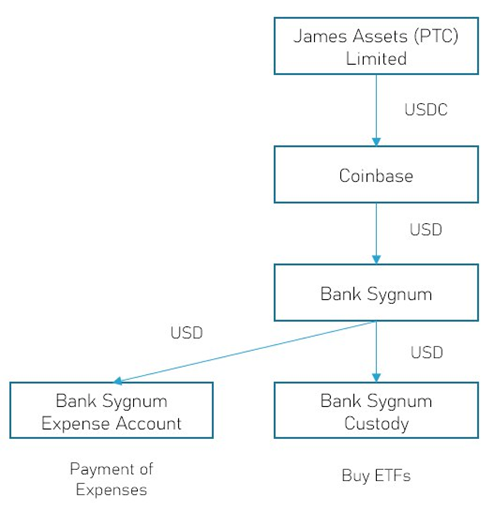

The trust operation flow is as below:

Figure 9: Operation flow of the trust, Source: DigiFT Research, MakerDAO MIP65

JAL acts as the holder of various bank accounts, and each transaction is initiated online. Approval from both Riverfront Capital (the sole director of JAL) and Hatstone (the transaction administrator of the trust) is required for each transaction.

Under this legal framework design, MIP65 of MakerDAO aims to achieve the following goals:

- No ability by third parties or Monetalis to access the funds or change the terms of the legal structure.

- Maker Governance has the complete ability to trigger a liquidation with a successful executive vote encoding an instruction to the trustee of the structure.

- It should not be possible for a single third party to block the ability of Maker Governance to make decisions or modify the structure.

- There must be no apparent weak links or edge cases that allow funds to get misappropriated or stuck.

- An asset purchase and allocation restriction, ensuring only appropriate bond assets and strategies can be acquired by the structure.

- All surplus generated by the legal structure must be manually sent to the Maker surplus buffer every quarter.

To achieve the inclusion of DAO-held RWA assets, MakerDAO has designed a complex trust structure and introduced new legal frameworks. As part of this design, $950,000 has been pre-allocated to Sygnum Bank for various expenses related to legal and trust services.

In addition, a recent community proposal called Project Andromeda was introduced at the end of May. This proposal suggests BlockTower as the project manager responsible for purchasing short-term U.S. government bonds on behalf of MakerDAO. The proposed debt ceiling for this project is $1.28 billion in Dai, further expanding MakerDAO's involvement in RWA assets. BlockTower has a history of collaboration with Centrifuge and MakerDAO, and the team also have extensive experience in traditional finance. Considering the successful implementation of Monetalis' processes, if MakerDAO is expected to significantly increase its engagement with RWA assets, this proposal has a high likelihood of being approved.

Tokenizing RWA into DeFi protocol – MakerDAO <> Centrifuge Stableswap

Centrifuge is a decentralized lending platform that provides a set of smart contracts to create a transparent market for the decentralized financing of RWA assets, eliminating unnecessary intermediaries. The goal of the protocol is to reduce borrowing costs for businesses while providing stable RWA collateralized income for DeFi users.

Currently, MakerDAO is the predominant purchaser of debt on the Centrifuge platform. However, Centrifuge is also working towards diversifying its buyer base. For example, Centrifuge is exploring the issuance of AAVE's stablecoin GHO using RWA assets as collateral within the AAVE community.

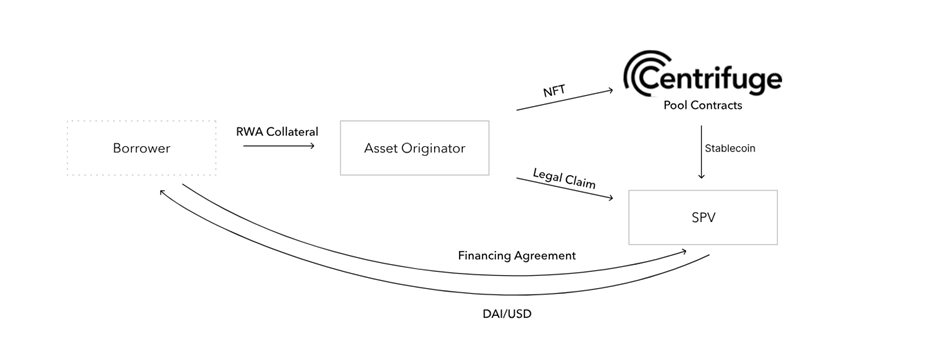

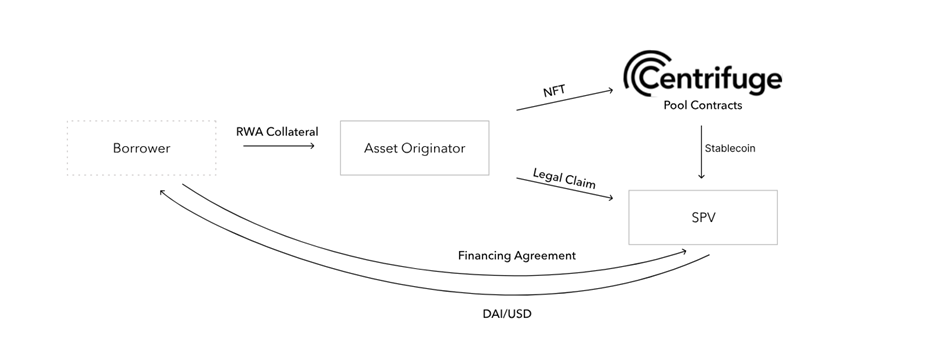

Figure 10: Centrifuge financing flow chart, Source: Centrifuge Docs

In fact, the process of issuing assets on Centrifuge is just like the process of issuing Asset-Backed Securities (ABS). The flow of funds operates as follows:

- The asset originator (such as BlockTower) creates a Special Purpose Vehicle (SPV) as the issuer, which serves as a separate legal entity for each fund pool, ensuring the independence of each pool. The Centrifuge contracts create corresponding fund pools on the Ethereum blockchain, which are associated with the respective SPVs.

- A borrower decides to finance their RWA, such as invoices or properties, by using them as collateral. The asset originator issues RWA tokens corresponding to the collateral and validates them. An NFT is minted as the on-chain representation of the collateral, with legal contracts associated with the assets.

- The borrower and SPV agree on the financing terms. The asset originator locks the NFT within the Centrifuge fund pool associated with the SPV and withdraws stablecoin Dai from the pool's reserves. This Dai can be transferred directly to the borrower's wallet or converted to USD and deposited into the borrower's bank account.

- On the maturity date, the borrower repays the financing amount and fees. They can choose to repay directly in Dai on-chain or initiate a bank transfer, which is then converted to Dai by the SPV and paid to the Centrifuge fund pool. Once all NFTs are fully repaid, they are unlocked and returned to the asset originator, where they can be burned.

The SPV is created by the asset originator, and the borrower typically has a business relationship with the asset originator.

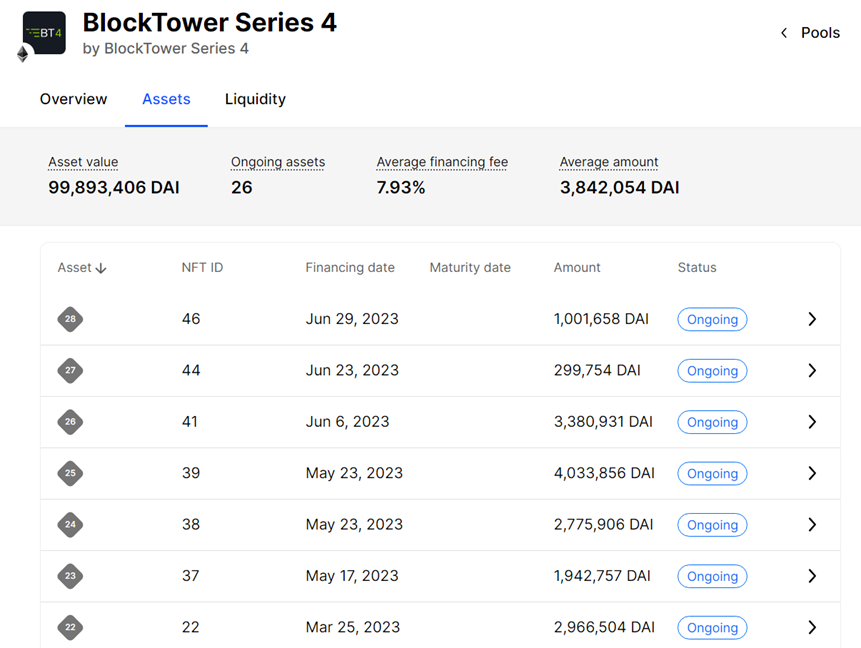

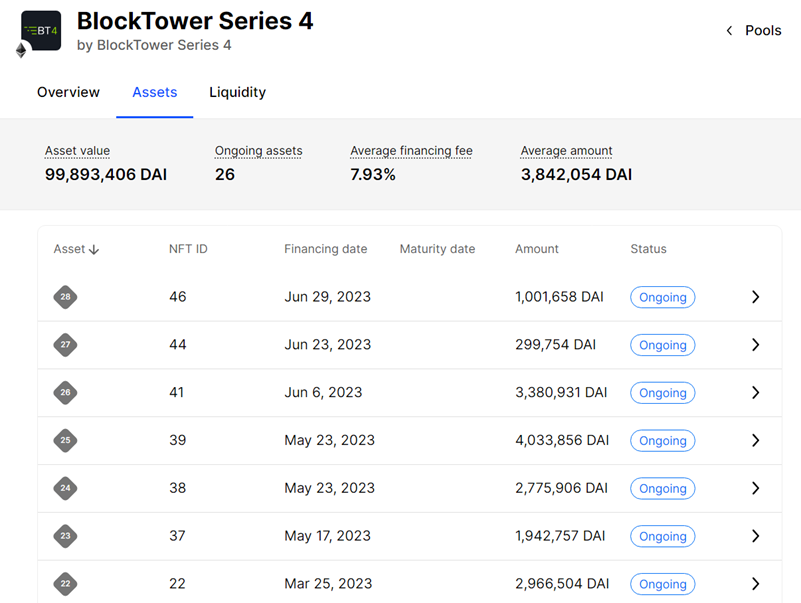

Figure 11: Part of the NFTs in Centrifuge BlockTower series 4 asset pool, Source: Centrifuge

The image shows the Centrifuge App page, specifically a screenshot of BlockTower Series 4. The list below displays NFTs that serve as on-chain collateral, with each NFT representing a RWA that has been verified by the asset originator. In this case, the assets are structured credits.

Centrifuge provides tools and a marketplace for projects/users who want to purchase RWAs directly, allowing assets to be integrated into the DeFi world while offering higher returns compared to typical stablecoin yields. However, there are risks involved, which come from Centrifuge itself and from borrowers acting as counterparties.

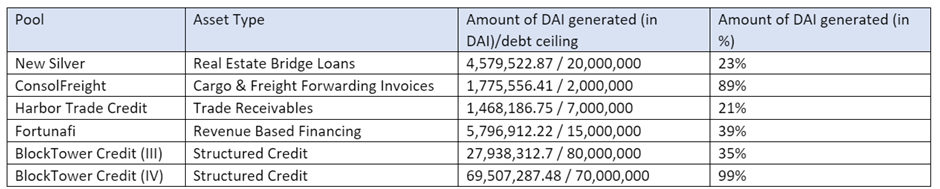

Figure 12: The amount purchased by MakerDAO on Centrifuge, Source: Daistats, data as of 2023.07.10

Currently, the loan data adopted by MakerDAO from Centrifuge is shown above. Compared to the Treasury Bill ETF project (Monetalis Clydesdale), the RWAs tokenized through Centrifuge have relatively smaller volumes, with the largest-scale BlockTower reaching just over a hundred million dollars. The advantage of this approach, compared to MakerDAO directly purchasing government bonds, is that it has a simpler process and does not require MakerDAO to build complex legal structures. In the recent community discussion, Centrifuge charges a fee of 0.4% to assist these projects in obtaining loans. MakerDAO does not incur any additional expenses in this regard. However, there is significant counterparty risk, and there is a possibility that these projects may default.

Conclusion

MakerDAO, as one of the largest DeFi projects, has explored two approaches in the integration of TradFi and DeFi in its community operations related to RWAs: direct purchase and holding of assets through DAO + trust (MIP65) and purchasing tokenized RWAs through Centrifuge. If we consider DeFi protocols' acceptance of RWAs, MakerDAO has the financial strength to establish an innovative legal framework directly, ensuring the safety of MakerDAO community assets and providing benefits to Dai and MKR holders. It pre-pays $950,000 in expenses and Monetalis charges an annual project management fee of 0.15% of the total amount. The other three companies involved in the trust will also incur respective expenses. Reports indicate that MakerDAO paid $2.1 million in expenses to Monetalis for the first phase of a $500 million government bond project in January 2023.

If we liken MakerDAO to a company and MKR tokens to company equity, it is intuitive to establish ownership rights and manage the treasury under traditional legal frameworks. However, the MKR token holders behind the scenes cannot be fully integrated into the existing corporate governance structures of the real world due to the nature of the DAO’s anonymity, lack of KYC, and different national and regional jurisdictions (subject to different laws and regulations). As a result, DAOs are fundamentally incompatible with the existing legal frameworks to ensure the safety of token holders' assets (especially RWAs), necessitating the design of the complex legal structuring set out above. The stability of this legal approach remains to be seen.

Most DeFi protocols and projects, do not have the resources, capabilities, and capacity to build a complete system. The second approach of directly purchasing tokenized assets is more feasible, especially if there are compliant asset issuers (traditional financial asset issuers typically require relevant licenses or permits). It only requires a simple community vote, followed by the purchase and transparent on-chain storage of the assets through multi-signature mechanisms. The risk primarily lies in the counterparty risk of the issuer. The market opportunity for RWA token issuance, as mentioned earlier, has seen a greater demand for bond-like RWAs in the medium term. Projects such as OpenEden, MatrixDock, Maple Finance, and Ondo Finance are exploring the tokenization of government bonds, as mentioned in the previous research report "Exploring RWA Use Cases: 5 Attempts at On-Chain U.S. Treasuries." According to DefiLlama data, the two projects with the highest RWA TVL also belong to government bond projects.

As DeFi development faces bottlenecks, the DeFi community has begun to further consider asset security. Previously, the focus was solely on smart contract vulnerabilities, but now there is increased attention to compliant assets. Traditional finance is inherently highly compliant, mitigating system risks caused by minor vulnerabilities through asset segregation, governance process and isolation, operation process standardization, and regulatory restrictions.

In the future, we can expect to see more protocols and projects incorporating RWAs into their balance sheets to achieve diversified asset allocation. In this context, compliant asset issuers will be indispensable, and better governance structures combining on-chain and off-chain elements will be gradually discovered and explored. We look forward to the transition from the virtual to the real world in the crypto space.

Reference:

Overview - Maker Endgame Documentation (makerdao.com)

Endgame Plan v3 complete overview - Legacy / Governance - The Maker Forum (makerdao.com)

Introduction to MakerDAO Collateral Onboarding - Collateral Onboarding

RWA (Real-World Asset) in MakerDAO - Innovation and Strategy in Fintech – MakerDAO (daogov.info)

Real-World Asset Report - 2023-05 - Maker Core - The Maker Forum (makerdao.com)

RWA Case Study - US T-bill Tokenization | DigiFT

MakerDAO - MIP65 - Monetalis Clydesdale (dune.com)

MakerDAO - Dashboard (dune.com)

About DigiFT

DigiFT aims to provide regulated decentralized finance solutions on the Ethereum public blockchain. We are operating the first regulation-abiding decentralized digital asset exchange where asset owners can issue blockchain-based security tokens efficiently and cost-effectively. Investors can trade with continuous liquidity via an AMM mechanism and retain control over digital asset tokens in their own wallets. We are a global outfit backed by well-established venture partners. The founding team originates from international financial institutions and has deep blockchain technology knowledge.

For more information, please contact:

Disclaimer:

This article and its contents are prepared solely for informational purposes only and do not replace independent professional judgement. Under no circumstances should the information contained herein be used or considered as an offer to sell, or solicitation of an offer to buy any security. The content of this presentation is proprietary and no part of it may be reproduced or redistributed without the prior written consent of DigiFT Tech (Singapore) Pte. Ltd. (“the Company”). This article contains public information as of the specified date and may be stale thereafter. No representation or warranty, express or implied, is made as to the fairness, accuracy or completeness of the article and the information contained herein and no reliance should be placed on it. None of the Company, its advisers, connected persons or any other person accepts any liability whatsoever for any loss howsoever arising, directly or indirectly, from this article or its contents. All information, opinions and estimates contained herein are given as of the date hereof and are subject to change without notice. This material should not be viewed as advice or recommendations with respect to asset allocation or any particular investment.

深度解读MakerDAO RWA 布局,DeFi 协议如何整合现实世界资产

TLDR

Web3 首先爆发的是固收类的产品,需求来自于 DAO 和 Web3 公司的财库管理。RWA 赛道占领 TVL 榜首的也均为国债代币化项目。

结合 RWA,让 DAO 组织的资产保留高流动性的同时,带来足够稳定、与链上活动相关性低的收益,实现更优质收入的同时分散风险。

DAO 的治理和运作并没有比传统公司结构更加高效。MakerDAO 通过复杂的而信托结构才能实现 DAO 对国债 ETF 的购买,成本高昂。

相比而言,由专业/合规的资产发行方将 RWA 代币化上链,由 DAO 组织购买是更加高效、可行的方式。

RWA 进入 Crypto 主流视野

在加密寒冬、美元加息的背景下,新一轮的 DeFi 创新将至未至,加密原生的DeFi 协议收益骤减,甚至其稳定收益率远低于美债 收益率—— 所谓的“无风险利率”。诸多 DeFi 项目把目光转向加密世界之外的现实世界资产(real-world assets, “RWA”)。在主流 DeFi 协议中,最早抢滩 RWA赛道 的是 MakerDAO。早在 2020 年,MakerDAO就以房地产开发担保贷款项目 6s capital 为抵押物构建 了RWA 金库,并与基于 RWA 的借贷平台 Centrifuge 合作,将抵押物代币化。MakerDAO 将这种代币列为稳定币Dai的抵押品之一,实现了抵押物构成的多元化。 MakerDAO 在 2022 年 5 月发布的 Endgame 计划中,也强调MakerDAO 构建去中心化稳定货币的其中一个关键部分是将RWA 作为抵押品。

近期各大 DeFi 协议在 RWA 赛道纷纷布局。2023 年6月, Compound 创始人 Robert Leshner创办新公司 Superstate,并向 SEC 提交申请,希望在以太坊上创建一个短期美国债券基金;MakerDAO 的 MIP65(MakerDAO Improvement Proposal, “MIP”, MIP65 为部署部分 MakerDAO 资金用于投资短期债券 ETF 的提议)在 今年5月通过新提案,将该金库上限从 5 亿美金提高到 12.5 亿美金,并将在未来数月内购买对应数量的债券 ETF。此外,包括高盛和花旗在内的多家传统金融巨头都表达了对RWA赛道的密切关注,并且不少已躬身入局。

Why now?

早在2018 年,作为RWA一个子集的 STO (Security Token Offering)曾在市场上引发过热潮,,但无疾而终。5 年后的今天,RWA叙事渐热。为什么是这个时间点?赛道的发展动力是什么?

- 基础设施角度:DeFi 基础设施逐渐完善。相关代币标准、预言机、周边开发工具更加齐全,有能力打通链上和链下;

- 资产和收益角度:Web3 原生资产触及瓶颈,资产基本同质化;熊市行情中链上活动低迷,缺乏Web3原生稳定收益来源;

- 叙事角度:CeFi 暴雷之后,投资者对风控和合规更为关注;传统金融领域高度合规,RWA 资产相对Web3原生资产,给投资者提供了更多保护;

- 监管及法规角度:监管在不断扩大边界,同时加密货币相关法律法规逐渐完善;

在上一轮行情中,类似模式的 RWA 平台初具雏形,如 Maple Finance,Clearpool,TrueFi 等。这类平台的基本模式是通过社区治理,为一些机构开放借贷资金池,用户投资资金池以获得预先约定的收益率,机构则可利用用该资金进行相关投资操作,并按照约定发放利息和归还本金。但早期的 RWA 平台缺乏合规流程和风险管理,在 Luna 和 FTX 暴雷后,,部分借款人破产导致无法归还借贷资产,导致投资者遭受严重损失。

图一:RWA 借贷协议活跃借贷金额,来源:rwa.xyz数据截至2023.07.06

从上图可以看出, 2022年 Luna 暴雷前,借贷金额达到顶峰,此后借贷量骤减。在 2022 年下半年由于 Luna 和 FTX 事件,损失最为惨重的是 Clearpool 和 TPS Capital,均在合规流程上存在重大失误。

TPS Capital 和 Clearpool 在 2022 年第二季度开始合作,在 Clearpool 上开设借贷资金池。TPS Capital 声称自身独立于 Three Arrows Capital,(Three Arrows Capital 在 Luna 事件后破产),。但最终 Three Arrows Capital 清算人准备的法庭文件显示二者的关联相当紧密复杂,Three Arrows Capital 实际上是 TPS Capital 的担保人,为后来TPS Capital违约的贷款提供担保。

2022 年 6 月 ,Clearpool 将 TPS Capital 的借贷池移除,同时 Clearpool 的数据合伙伙伴 X-Margin 将 TPS Capital 的评级降至 B,借贷上限降低为 0 美元。Clearpool 和 X-Margin 宣布将合作确保 TPS Capital 归还借贷资金,确保用户不遭受损失。

雪崩之前世界一片寂静,直到最后一片雪花落下。这些数千万美元的损失都是惨重的前车之鉴,也让想参与RWA赛道 的开发者更加关注风险控制、合规流程和法律框架。

什么是 RWA?

RWA 指各种存在于区块链之外,但可以通过一定方式代币化上链和现有 DeFi 协议结合的资产。目前主要的 RWA 项目主要集中于下述几种类型:

债券,包括私人债券、公司债券和国债

- 股权

- 房地产

- 高价值的收藏品

- 碳信用积分

我们认为最早能够进入 DeFi的是债券型产品,包括国债和公司债券产品,需求侧以 DeFi 协议对 RWA 的采纳和 Web3 协议国库管理为主。根据 DefiLlama 数据,目前 RWA 项目中,TVL 位居前二的为美债代币化平台(OpenEden 和 MatrixDock),其次为房地产相关 RWA 平台(Tangible 和 RealT)。但总计数亿美金的体量,不论是和 DeFi 还是和整个 Tradfi 领域相比都还比较小,存在巨大的成长空间。

图二:RWA 项目TVL,来源:DefiLlama,数据截至 2023.07.10

RWA 的动力来源

总的来说,现有 DeFi 协议主要将 RWA 资产应用于三种途径:1)金库资金管理,部分 MakerDAO 的 RWA 的需求来自于此;2)用作抵押品,如 MakerDAO 和 Solana 生态稳定币协议 UXD Protocol;3)为 DeFi 场景引入新的资产类型,如 Curve(MatrixDock STBT)和 Flux Finance (Ondo Finance OUSG)。

DeFi 协议引入 RWA 有多种动力来源,包括:

- 链上资管需求

- 链上资管寻求稳定收益和较好的流动性,现实世界中的国债等产品是被广泛认可的投资标的,其收益相对稳定,且流动性非常可观,属于达到万亿美元市值的资产类别。

- 替代性收益来源

- 链上原生收益主要来自于Staking/Trading/Lending,当加密市场波动较大,在行情低迷时,链上金融活动活跃度下降将导致收益下跌。如当前的市场状态下,主流链上平台收益甚至低于美国国债。若寻求与链上原生资产相关性较低的替代性收益,引入 RWA 相关资产无疑是一种好的选择。

- 分散投资组合

- 链上资产种类相对单一,且具有高度相关性和较高的波动率。引入更稳定、并和链上原生资产相关性很低的 RWA 资产可实现对冲目的,构成更丰富有效的投资组合策略。

- 引入多元化抵押品

- 链上资产的高度相关性,导致借贷协议容易发生挤兑或是大规模的清算,从而进一步加剧市场波动;引入和链上资产相关性较低的 RWA 资产可以有效缓解此类问题。

下面我们以 MakerDAO 为例,来详细分析 DeFi 协议如何应用 RWA(作为抵押物)。

MakerDAO RWA应用深度探析

MakerDAO是一个去中心化自治组织(DAO),旨在创建和管理基于以太坊的稳定币 Dai。用户锁定以太坊(ETH)作为抵押物,生成Dai稳定币。Dai的目标是与美元保持1:1的锚定关系,通过智能合约和算法稳定其价值。由于加密货币市场的高波动性,单一抵押物容易导致大规模清算,因此 MakerDAO 一直在尝试将其抵押物多元化,引入 RWA 就是重要手段之一,甚至写入了 MakerDAO Co-founder Rune Christensen 提出的 Endgame 计划中。

图三:Dai 当前现状,来源:daistats.com,数据截至 2023.07.10

上图展示了当前 Dai 的总量(约 46.5 亿),MakerDAO 设定的上限为 62 亿。目前Dai的抵押品组成已经实现相对多元化,囊括了部分 RWA 和各类稳定币。

单一抵押物的风险

2020 年 3 月 12 日,由于疫情引发的金融危机导致金融市场崩溃,美股市场连续熔断。作为金融市场的一个边缘细分市场,加密货币市场更是急速下跌,作为以太坊链上头部 DeFi 协议之一 MakerDAO 也受到了巨大的冲击。一方面,由于以太坊网络容量有限,网络拥堵,清算者无法及时对风险账户进行清算;另一方面,部分稳定币 Dai 的借款人需要购买 Dai 来偿还债务,取出抵押的资产,导致市场对 Dai 的需求增加,进一步加大清算难度。多重因素下, MakerDAO 出现规模达 567 万美元的坏账。最终 MakerDAO 只能于2020 年三月下旬通过增发 20980 枚 MKR 代币筹集 530 万美元来弥补坏账。

MakerDAO Endgame计划

在经历此类事件之后,MakerDAO 也不断尝试将抵押物多元化,MakerDAO 系统目标是逐步建立去中心化的稳定货币,而构建货币系统,需要以当前具备共识的资产作为抵押物,借用其信用。原生加密货币自然是抵押物的重要组成部分,但本质上加密原生资产具有高度相关性,仅仅通过加密资产很难实现抵押物的多元化。为分散当前加密货币市场的风险,MakerDAO 引入了部分 RWA 资产作为稳定币 Dai 的抵押物。

MakerDAO Endgame是 MakerDAO 联创 Rune Christensen 于 2022 年 5 月提出的一系列 MakerDAO 未来设想和计划,其中对于构建去中心化稳定货币的路径做了规划。这最终需要两种类型的抵押物:可以在物理上保证公正特性的去中心化资产,以及可以提供可靠流动性和稳定性的真实世界资产。同时还要展示 DeFi、Maker和Dai稳定币能为世界带来的好处,让世界经济体系逐步和 DeFi 融合并采纳 Dai 作为支付和结算工具。

Endgame 计划分为三个阶段,三个阶段以抵押物成分来划分,最终将 Dai 打造成稳定货币:

- 鸽态(当前状态):对于RWA 作为抵押物没有限制,稳定币 Dai 保持和美元的锚定

- 鹰态:Dai目标利率为负,自由浮动

- 凤凰态:稳定币 Dai 的抵押物中除了具有物理弹性 RWA以外不再有其他类型的 RWA

在具体规划中设计了每个阶段对应抵押物的具体比例,可参考原文,在此不多赘述。

Endgame Plan v3 complete overview - Legacy / Governance - The Maker Forum (makerdao.com)

当前 MakerDAO RWA 的成分

纵观货币历史,人类采纳的货币从早期的商品货币,采用某种形成共识的稀缺资源作为等价物,如贝壳、黄金等,到后来以具备共识的稀缺资源作为抵押物发行纸币,如储备黄金发行纸黄金,发展到当前以军事实力为基础发行的信用货币,如美元。MakerDAO 的 Dai 虽然有数十亿的体量,但从更大的维度来看还是沧海一粟,它需要借用其他资产的信用,凸显自己的优势来逐步巩固地位。在 MakerDAO 联合创始人提出的 Endgame 计划中,也引入 RWA 作为过渡:在加密资产世界还不够坚实的情况下,需要现实世界资产为锚。根据 MakerBurn 的数据,目前共计有11 个 RWA 项目,21.2 亿美金的资产作为 MakerDAO 的抵押物。

图五:MakerDAO RWA 抵押数据,来源: MakerBurn.com, 数据截至 2023.07.10

根据 Dune 数据面板显示,这些 RWA 资产带来的收益大幅度增加了 MakerDAO 的利润。目前 RWA 占 MakerDAO 总资产的 40% 左右,贡献超过 50% 的收益。

图六: MakerDAO 资产构成,来源:Dune.com,数据截至2023.07.10

右侧中间蓝色部分为 RWA 占比,目前占比 41.5%。

图七: MakerDAO 协议利润, 来源: Dune.com,数据截至2023.07.10

MakerDAO 的协议利润组成中,右上方为来自 RWA 的利润,占比 51.1%。由此,MakerDAO 在 2023 年6 月通过提案,将Dai Saving Rate(Dai 的无风险利率)从 1% 提高到了 3.49%,为 Dai 持有者提供了有吸引力的收益。

从类型上来划分,MakerDAO 的 RWA 主要包括四个部分:

- 编号 RWA 001,6s capital,提供房地产贷款。

- MIP81,编号RWA014,由 Coinbase Institutional 在 2022 年 9 月提出的 Proposal,将部分 MakerDAO 持有的 USDC 投入 Coinbase USDC Institutional Rewards,提供 1.5% 基于 USDC 的 APY。

- 来自去中心化借贷平台 Centrifuge 实现代币化后的资产,由 MakerDAO 购入相关代币,其中包括 New Silver(房地产借贷),BlockTower(结构化信贷) 等。

- MIP65,名称为 Monetalis Clydesdale,编号 RWA007,由 Monetalis 提出,将 MakerDAO 持有的稳定币用于购买短期债券 ETF,在 2022 年 10 月首次通过提案(5 亿美金),后在 2023 年 5 月通过提案将债务上限提高( 至12.5亿美金)。

其中 6s capital 和 Coinbase 是单独的合作案例,本文将着重于Centrifuge和 Monetalis Clydesdale 部分,来探讨 DeFi 协议如何结合 RWA。涉及的相关问题不仅仅是技术方案和商业模式,更关系到治理架构、法律框架和资产确权等。

DAO如何购买国债?MakerDAO 的 Monetalis Clydesdale 项目

MIP65,名称为 Monetalis Clydesdale, 由 Monetalis 的创始人 Allan Pedersen 在 2022 年 1 月提出,在 2022 年 10 月通过并执行,目标是将 MakerDAO 持有的部分稳定币投资于高流动性、低风险的债券 ETF 中,初始债务上限为5亿美金,并在 2023 年 5 月通过后续提案将上限提高到 12.5亿美金。

在 2022 年2 月份提出的 MIP13 中社区的讨论,在当时 MakerDAO 的资产负债表中约 60% 是各类稳定币(以 Peg Stability Module(“PSM”)机制来确保 Dai 的价值稳定,储备以 USDC 为主),并在过去 18 个月都由超过50% 的资产为稳定币,却没有为 MakerDAO 创造利润。其中对手方风险主要来自于 Circle(USDC 发行方),社区希望通过一些方式将稳定币投资出去,获取利润并分散风险,其中就有提出投资短期美国国债的想法。

随后在参与 MIP65 提案投票的 MKR 代币持有者中,71.19% 支持该提案,最终得到通过。 MIP65 将会启动一个 RWA 相关的金库,将 MakerDAO PSM 机制中的资金通过信托的形式投入到高流动性的债券策略中。

其中,Monetalis 是由 Allan Pedersen 和 Alessio Marinelli 创办的咨询公司,为传统金融和 DeFi 机构提供咨询服务和解决方案。两位创始人都在传统金融、咨询和风险投资机构中有丰富的经验。Monetalis 的投资人包括 UDHC,Dragonfly 和 MakerDAO 联合创始人 Rune Christensen。

该提案整体业务架构如下:

- MakerDAO 通过投票委托 Monetalis 设计整体架构,Monetalis 需要周期性向 MakerDAO 汇报

- Monetalis 作为项目规划和执行者,设计整体信托的架构,其中

- Riverfront Capital(SHRM Trustee (BVI) Limited )是唯一董事(director).

- Hatstone(Fiduciary Group Limited) 作为交易的管理人,信托的交易需要由该公司批准.

- Belvaux Management Ltd 作为信托执行人,确保信托按照目标运行.

- MakerDAO MKR 代币持有人为整体受益人,能够通过治理指示信托资产的购买和处置;

- James Asset (PTC) Limited ( “JAL” )为受托人;

- Coinbase 提供USDC 和 USD 的兑换服务.

- Sygnum Bank 提供信托资产的交易和托管,并另设账户用于信托运行的开销.

- 资金用于投资两类 ETF 产品,分别为 Blackrock 的 iShares US$ Treasury Bond 0-1 yr UCITS ETF 和 Blackrock 的 iShares US$ Treasury Bond 1-3 yr UCITS ETF

其中:

- JAL 是持有信托的壳(shell company),是在 BVI新建立的公司

- Riverfront Capital(SHRM Trustee (BVI) Limited) 是 1990 年代成立的公司,提供专业的信托服务。

- Hatstone (Fiduciary Group Limited)有超过10亿美元的资产总量,提供资金管理、企业服务、基金投资等服务。

- Monetalis 在 MakerDAO 的委托下作为项目管理人,设立整体架构。Monetalis 的情况不会影响到 MakerDAO 的资产。Monetalis 每年会收到0.15%的管理费,按季度支付.

- Sygnum Bank是全球首家受监管的数字资产银行,也是一家具有全球覆盖能力的数字资产专家,总部位于瑞士和新加坡。其产品包括受监管的加密货币交易。凭借Sygnum Bank AG在瑞士的银行执照以及Sygnum Pte Ltd在新加坡的资本市场服务(CMS)许可证,Sygnum使机构投资者、合格的私人投资者、企业、银行和其他金融机构能够完全信任地投资于数字资产经济。

图八: Monetalis 项目信托架构,来源:DigiFT Research

购买流程图如下:

图九: 信托运作流程图,来源: DigiFT Research

其中 JAL 是各个银行账户的持有人,每一笔交易都在线上发起,需要同时通过 Riverfront Capital(JAL 的唯一董事)和 Hatstone(JAL 的交易管理人)的审批。

在这样的法律架构设计下,MakerDAO MIP65 能够达成的目标有:

- 第三方或 Monetalis 没有能力改变法律条款,也不能接触到相关资金

- 通过信托,MakerDAO MKR 的持有人有能力通过社区投票和治理触发清算

- 没有单一第三方有能力阻碍 MakerDAO 对该信托的治理,或是修改条款

- 不能有任何明显的弱点或特殊情况,导致资金被挪用

- 确定该信托结构只能购买规定的资产类型和金额

为实现 DAO 持有的 RWA,MakerDAO 设计了复杂的信托结构和全新的法律条例,并随之有高昂的开销,包括初始用于各项费用的 95 万美金,以及后续为信托相关的各个机构和项目管理人 Monetalis 持续支付的费用。

此外,MakerDAO 最新社区提案中,在五月底社区成员提出了 Project Andromeda,由 BlockTower 作为项目管理人,购买短期美国国债,债务上限为 12.8 亿美金的 Dai,进一步增加 MakerDAO RWA 方面的投入。BlockTower 通过 Centrifuge 和 MakerDAO 有多次合作,团队也在传统金融有丰富的经验,加上 Monetalis 跑通的流程在前,若 MakerDAO 社区希望仅以增加 RWA 方面的投入,该提案有很大可能性被通过。

代币化资产纳入 DeFi 协议 – MakerDAO <> Centrifuge

Centrifuge 是一个去中心化借贷平台,提供一系列智能合约来创建一个透明的市场,无需不必要的中介机构,实现链上对 RWA 资产的去中心化融资。该协议的最终目标是降低企业的借贷成本,同时为 DeFi 用户提供稳定的 RWA 抵押品收益来源。

图十:Centrifuge 资金运行图,来源: Centrifuge 文档

实际上 Centrifuge 上发行资产的流程接近 ABS(Asset-Backed Securities)发行的流程。资金运行

流程如下:

- 资产发起方(asset originator,如 BlockTower)创建一个特殊目的实体(SPV,作为发行方,issuer),作为每个资金池的独立法律主体,保持每一个资金池的独立;Centrifuge 的合约会在以太坊上创建对应的资金池,并与对应的 SPV 关联起来;

- 借款人(borrower)决定以一些现实世界资产作为抵押物进行融资,这些资产可以是发票或是房产;

- 资产发起方发行该抵押物对应的 RWA 代币,进行验证,并铸造对应的 NFT 作为链上抵押品;

- 借款人和 SPV 就融资条款达成协议;资产发起方将 NFT 锁定在于 SPV 相关的 Centrifuge 资金池中,从该池的储备中提取稳定币 Dai;Dai 可以直接转入借款人的钱包,或由 SPV 转换为美元进入借款人对应的银行账户;

- 借款人在 NFT 到期日偿还融资金额和费用,可以选择链上以 Dai 直接还款,或是通过银行转账,再通过 SPV 转换为 Dai 支付给 Centrifuge 资金池;一旦所有 NFT 完全偿还,他将解锁并归还给资产发起方,可以被销毁。

其中 SPV 由资产发起方创建,借款人一般和资产发起方有业务联系。

图十一:Centrifuge BlockTower series 4 部分资产, 来源:Centrifuge

图为 Centrifuge App 页面,其中 BlockTower Series 4 的截图,下方列表为作为链上抵押品的 NFT,每个 NFT 对应一笔由资产发起方验证过的链下现实资产,在该案例中为结构化信贷。

Centrifuge 为需要购买 RWA 的项目方/用户提供了直接购买 RWA 的工具和市场,能够将资产嵌入 DeFi 世界,同时提供相比市场一般稳定收益率更高的收益,但也存在一定的风险,风险来自于作为对手方的借款人。

数据:MakerDAO 购买的 Centrifuge 平台资产类型和数量,以及以此为抵押发行 Dai 的数量,来源:Daistats,数据截至 2023.07.10

目前 MakerDAO 采纳的几个来自 Centrifuge 的借款数据如上,相比国债项目,通过 Centrifuge 代币化的 RWA 相对体量较小,最大规模的 BlockTower 整体也刚达到上亿美金。相比 MakerDAO 直接购买国债,该方案的优势在于流程简单,也不需要 MakerDAO 本身去搭建复杂的法律架构。在最近的社区讨论中,Centrifuge 会抽取 0.4% 的费用来帮助这些项目获得贷款;MakerDAO 在其中不需要承担额外的费用。但由于这些项目相比国债有更高的违约可能性,整体存在更大的对手方风险。

结论

MakerDAO 作为体量最大的 DeFi 项目之一,在数年 RWA 相关的社区运作中同时尝试了两种形式:通过 DAO + 信托的形式直接购买和持有资产(MIP65)和购买代币化 RWA(通过 Centrifuge),是目前将 Tradfi 和 DeFi 结合的最好案例。

相比其他规模较小的 DeFi 协议,MakerDAO 有足够的资金实力来实现 DAO 对国债的直接购买,但成本高昂。其中 MakerDAO 设立了一个创新型的法律架构,通过一个复杂的信托结构,来确保 MakerDAO 社区的资产安全,为 Dai 和 MKR 代币持有人带来 RWA 的收益。为此 MakerDAO 预先支付了 95 万美金的开销,此外,Monetalis 需要每年收取总金额的 0.15% 作为项目管理费用,其余三家参与信托的公司也有对应的开销。有报道支出,MakerDAO 该项目在 2023 年 1 月为第一期 5 亿美金的国债 ETF 购买支付了约 210 万美金的开销。这对于普通 DeFi 项目来讲成本过高。

追溯原因还是在于MKR 代币背后持有人无法完整映射到现实世界的法律框架中,匿名、无 KYC、归属不同国家和地区(需要遵守不同的法律法规),也就无法和现实世界现有的法律框架兼容,来确保代币持有人资产(特别是链下资产)的安全性,因此设计如此复杂的法律框架来实现国债 ETF 的购买。该法律框架是否会出现问题,还有待考察。

对于大多数 DeFi 协议和项目方而言,他们并没有精力、资源和能力构建一套完整的体系。第二种直接购买代币化资产的方式会更容易,若有合规的资产发行方(传统金融资产发行都需要持有相关牌照或许可),仅需要简单的社区投票,购买之后通过多重签名保存资产在链上,并将地址公开由社区监督即可,风险更多在于发行方的对手方风险。RWA代币发行的市场机会,如前文所提,中短期对债券类 RWA 的需求会相对较多,最先崛起的是国债类项目,如此前的研究报告《RWA 应用案例探讨:链上美债的 5 个尝试》种提到,OpenEden,MatrixDock,Maple Finance、Ondo Finance 等都在做国债代币化的尝试,根据 DefiLlama 数据,RWA TVL 最大的两个项目也属于国债类项目。

在DeFi 发展遇到瓶颈的情况下,DeFi 社区也开始进一步考虑资产安全问题,从以往仅担心智能合约漏洞,进一步到关注合规资产;传统金融原本就是高度合规,通过资产隔离、治理角色分配和隔离、流程标准化、制度限制等,避免出现细小漏洞而导致大规模的系统风险。

预期未来我们会看到更多的协议和项目将 RWA 纳入资产负债表,实现多元化资产配置,在这里,合规的资产发行方会不可或缺,以及更好的链上链下结合的治理结构也会逐步被发现和探索。期待加密世界的脱虚向实。

参考文献

Overview - Maker Endgame Documentation (makerdao.com)

Endgame Plan v3 complete overview - Legacy / Governance - The Maker Forum (makerdao.com)

Introduction to MakerDAO Collateral Onboarding - Collateral Onboarding

RWA (Real-World Asset) in MakerDAO - Innovation and Strategy in Fintech – MakerDAO (daogov.info)

Real-World Asset Report - 2023-05 - Maker Core - The Maker Forum (makerdao.com)

RWA Case Study - US T-bill Tokenization | DigiFT

MakerDAO - MIP65 - Monetalis Clydesdale (dune.com)

MakerDAO - Dashboard (dune.com)

关于 DigiFT

项目介绍: DigiFT 由张之皓——前华美银行大中华区首席执行官、花旗银行和渣打银行中国区副行长,于 2020 年创立,其管理团队在传统金融机构和金融科技领域拥有丰富经验。 DigiFT 的愿景是整合中心化与去中心化金融的优势,是目前第一家,同时也是唯一一家进入新加坡金融管理局(MAS)金融科技监管沙盒的去中心化交易所。DigiFT 在以太坊公链上提供符合监管的去中心化金融方案,部署自动做市商(AMM)机制,促进由债券、股权等金融资产作为底层支持的证券型通证的二级市场交易流动性。

更多信息,请联系:

免责声明:

本文及其内容仅供信息目的使用,不替代独立的专业判断。在任何情况下,本文所包含的信息不应被视为出售或购买任何证券的要约或征求。未经 DigiFT Tech (Singapore) Pte. Ltd.(“公司”)事先书面同意,任何部分均不得复制或重新分发。本文包含的公开信息仅截至指定日期,并可能在此后过时。对于文中和其中所包含的信息的公正性、准确性或完整性,不作任何明示或暗示的陈述或保证,不应依赖于此。公司、其顾问、关联人员或任何其他人对于由于本文或其内容而直接或间接引起的任何损失概不承担任何责任。本文中所包含的所有信息、观点和估计均截至本日期,并且可能随时变动,恕不另行通知。本材料不应被视为关于资产配置或任何特定投资的建议或推荐。