“比特币现货 ETF 临近,加密货币合规产品现状如何?”

下载报告(中文) - PDF

The Market Wakes Up

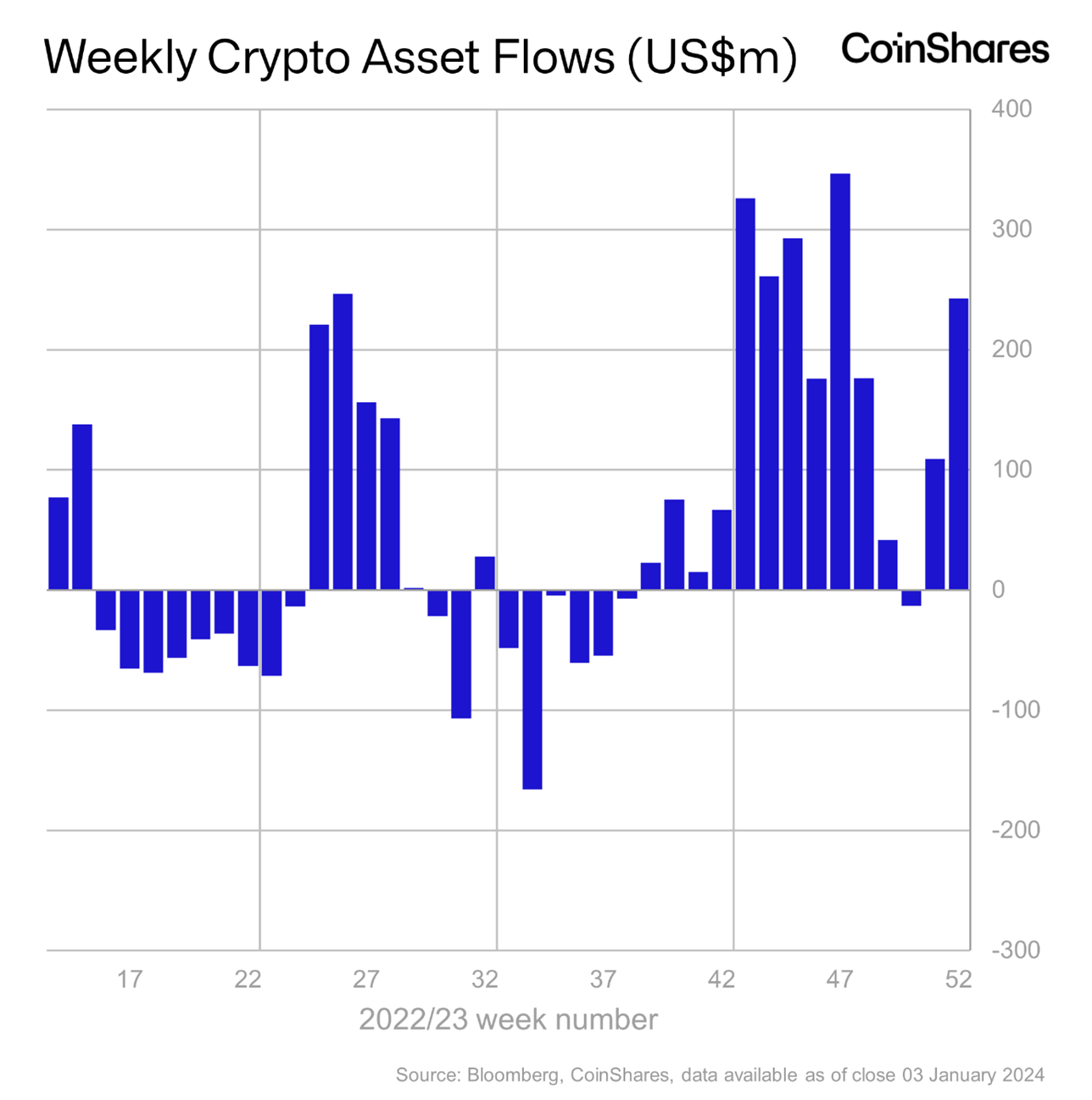

As cryptocurrencies have gradually entered the mainstream spotlight over the past decade, the influx of funds from traditional markets, starting with Grayscale's GBTC, has increasingly garnered attention in the cryptocurrency market. The recent market resurgence is closely tied to traditional institutions. According to CoinShares' weekly data on cryptocurrency asset flows (Data of crypto asset ETPs on various traditional trading venues), there has been a continuous net inflow for over ten weeks since early October 2023, with only a small amount of outflow in one week in December 2023. Bitcoin's price has also surged from around $25,000 to over $45,000.

The market widely believes that this reflects investors' anticipation of the U.S. SEC approving application for offering Bitcoin spot ETFs from several traditional asset management giants in January 2024. Based on the historical ETF approval process, the SEC's maximum timeframe for final approval is 240 days. As Hashdex and Ark&21 Shares were among the first institutions to submit ETF applications to the SEC, the expected deadline for approval is January 10, 2024. The market believes that if the application for offering Bitcoin spot ETF is approved, there is a high probability that subsequent ETFs from other institutions like BlackRock, Fidelity, etc., will also likely receive approval.

Before the application of offering Bitcoin spot ETFs in the United States, the capital market has long had compliant channels for exposure to cryptocurrency assets. As early as 2013, Grayscale's GBTC was launched, allowing investors to purchase shares of the GBTC trust through traditional brokerage channels, indirectly holding Bitcoin and other cryptocurrency assets.

Over the past few years, Europe has seen the launch of over a hundred ETPs related to cryptocurrency assets on traditional trading venues, enabling investors in the region to acquire cryptocurrency assets through conventional channels.

Asset management giants also launched and traded their own Bitcoin Spot ETFs on exchanges outside US. For example, Fidelity’s Bitcoin spot ETF, ticker FBTC, is listed and traded on the Toronto Stock Exchange (TSX) in Canada.

Why is there such a focus on the U.S. Bitcoin spot ETF? How does it differ from existing compliant channels for purchasing cryptocurrency assets?

The Current status of regulatory-compliant cryptocurrency asset investment channels

We analyzed the products issued by major institutions, as compiled by CoinShares, a digital asset provider. CoinShares provides weekly data on the global flow of funds into compliant cryptocurrency products across various regions. These products are based on cryptocurrency assets and are traded through traditional financial channels, including various types of ETPs and trust products. The following data, as of December 31 2023, reflects the flow of funds from traditional finance, particularly institutional investor funds, into cryptocurrency assets.

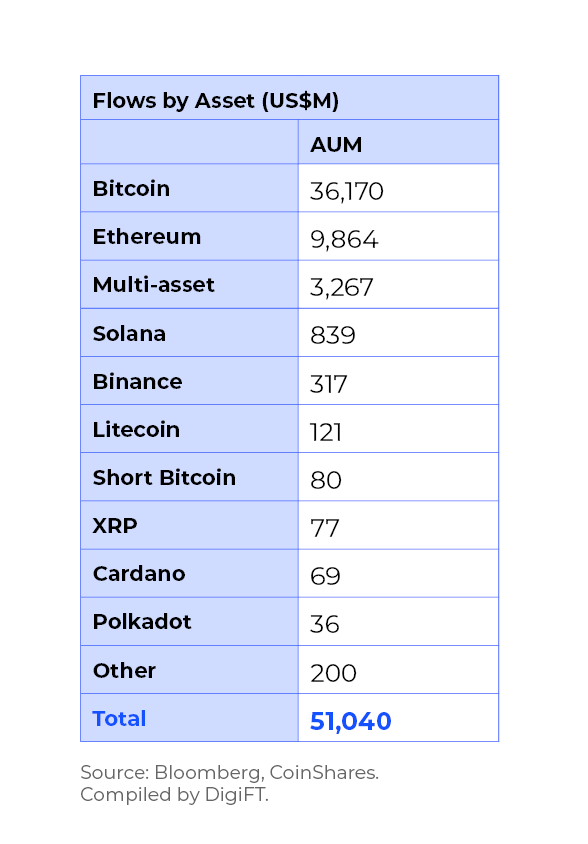

The assets primarily invested through these channels include:

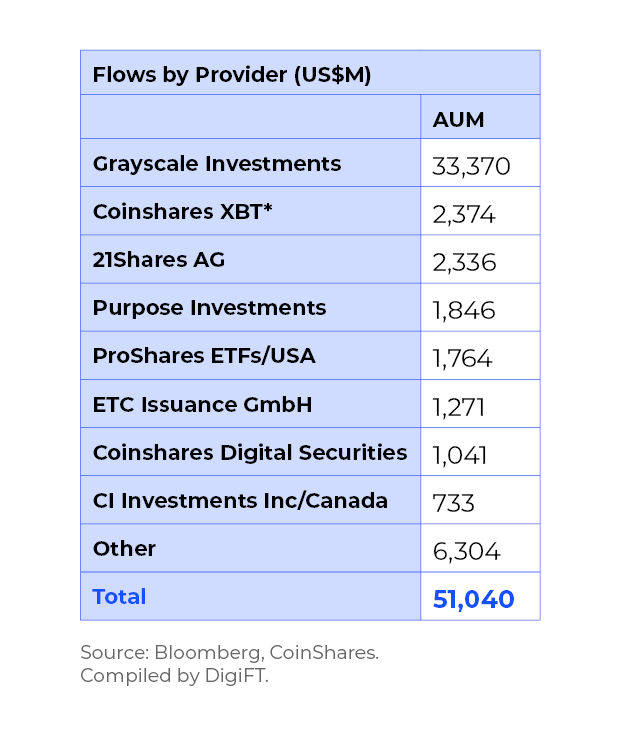

The main asset providers are:

Among them, the background and product structure of the top five asset management issuers are as follows:

Grayscale Investments LLC

- Intro: Grayscale Investments is an American digital currency asset management company and subsidiary of Digital Currency Group founded in 2013 and based in Stamford, Connecticut. Grayscale launched its Bitcoin Trust GBTC in 2013.

- Major Product: Grayscale Bitcoin Trust (GBTC)

- Product legal structure: trust (physically backed)

- Fee: 2% management fee

- Trading platform: OTCQX

- Inception date: 2013.09.25 (inception date)

- Investor requirement: qualified investors and institutional investors

- Crypto asset product AUM:33,370 million USD (data as of 2023.12.31)

CoinShares XBT

- Intro: XBT Provider by CoinShares is Europe’s first entity to offer investors easy exposure to Bitcoin and Ethereum without the burden and risks of self-custody. CoinShares is a leader in the cryptocurrency Exchange Traded Products (ETP) industry, offering innovative, reliable products to investors seeking a convenient and trustable way to access a diverse range of digital assets.

- Major product: Bitcoin Tracker One (COINXBT SS)

- Product legal structure: Tracker certificates (Synthetic backed)

- Fee: 2.5% management fee

- Trading platform: Nasdaq Stockholm

- Inception date: 2015.05.18

- Investor requirement: Nordic retails

- Crypto asset product AUM: 2,374 million USD (data as of 2023.12.31)

21 Shares AG

- Intro: 21Shares is the world's largest issuer of crypto exchange-traded products (ETPs), established in 2018. 21Shares AG is based in Zurich, Switzerland. Its products include the first physically backed Bitcoin and Ethereum ETP.

- Major product: 21Shares Bitcoin ETP(ABTC)

- Product legal structure: Debt security (physically backed)

- Fee: 1.49% management fee

- Trading platform: SIX Swiss exchange

- Inception date: 2019.2.25

- Investor requirement: Nordic retails

- Crypto asset product AUM: 2,336 million USD (data as of 2023.12.31)

ProShares ETFs

- Intro: ProShares has been at the forefront of the ETF revolution since 2006. ProShares now offers one of the largest lineups of ETFs, with more than $64 billion in assets. The company is the leader in strategies such as dividend growth, interest rate hedged bond and geared (leveraged and inverse) ETF investing.

- Major product: Bitcoin Strategy ETF(BITO)

- Product legal structure: future ETF (Synthetic backed)

- Fee: 0.95% management fee

- Trading platform: NYSE Arca

- Inception date: 2021.10.18

- Investor requirement: US retails

- Crypto asset product AUM: 1,846 million USD (data as of 2023.12.31)

Purpose Investments Inc ETFs

- Intro: Purpose Investments is an asset management company with more than $18 billion under management. Purpose Investments has an unrelenting focus on client-centric innovation and offers a range of managed and quantitative investment products.

- Major product: Purpose Bitcoin ETF (BTCC)

- Product legal structure: Spot ETF (Physically backed)

- Fee: 1.00% management fee

- Trading platform: TSX

- Inception date: 2021.2.25

- Investor requirement: North American retails

- Crypto asset product AUM: 1,764 million USD (data as of 2023.12.31)

ETF, ETP, Trust, what’s the difference?

According to the legal structure of products, compliant cryptocurrency products in the market can currently be classified into Exchanged Traded Products (ETPs) and Trusts. Meanwhile, ETP can be classified into Exchange Traded Notes (ETNs), Exchange Traded Funds (ETFs), and Exchange Traded Commodities (ETCs). In cryptocurrency assets related ETPs, most are ETNs and ETFs.

Among them, ETFs can provide better accessibility for investors, allowing simultaneous investment in multiple assets, with lower fees and suitability for long-term investments. However, ETFs may experience tracking errors, where the value of assets in the ETF differs from the benchmark it is supposed to track, ultimately leading to returns lower than expected. Some other drawbacks of ETFs are their liquidity concerns, complicated creation and redemption process, tax issues, etc.

ETNs are a debt structure, typically unsecured debt instruments issued by financial institutions. Investors purchase the issuer's debt, which poses higher risks due to credit concerns. Compared to ETF structures, ETNs generally have poorer liquidity. However, the advantage of ETNs lies in providing more diversified asset types without the tracking error issue, and they offer more flexibility in terms of taxation. Among the mentioned products, 21Shares Bitcoin ETP is a typical example of an ETN product.

The trust structure is relatively complex and generally can only be traded in the OTC market. For example, Grayscale's GBTC trades exclusively on OTCQX, a platform with lower liquidity and fewer investors. The total daily trading volume on the platform only reached $1.3 billion (as of January 2, 2024). Additionally, Grayscale GBTC, issued through a trust structure, allows only one-way subscriptions and cannot be redeemed. Investors can acquire the issued shares six months after subscribing and then trade them on the secondary market. This nature contributes to GBTC experiencing positive premiums in bull markets and negative premiums in bear markets.

Furthermore, the above-mentioned products, based on the classification of underlying assets, can be divided into two categories: physically backed and synthetically backed.

Physical ETPs physically buy and hold the underlying assets they are designed to track, such as stocks, cryptocurrency, or commodities. The performance of a physical ETP is therefore directly linked to the performance of the underlying asset(s). For example, Purpose Investment’s BTCC, is a BTC spot ETF traded on TSX. Each share of the ETF has a certain amount of Bitcoin managed by the fund manager. Usually there will be a custodian for holding the Bitcoin. Here the custodians of BTCC are Gemini Trust Company and Coinbase Trust Company

Synthetic ETPs use swap agreements with a counterparty, typically a bank, to provide the return of the underlying assets. To ensure the return is delivered each day, the swap counterparty is often required to deposit liquid and diversified collateral (usually in the form of treasuries or blue-chip equities) with the issuer, held by an independent custodian. The amount of collateral required fluctuates with the value of the asset the ETP is designed to track. For example, ProShares’ BITO is a bitcoin future ETF listed on NYSE. The ETF invests in bitcoin future contracts on CME.

The impact of SEC’s approval on Bitcoin Spot ETF

The various types of cryptocurrency financial products traded through traditional financial channels mentioned above provide investors with a one-stop channel to gain exposure to cryptocurrency assets. This bypasses the technical and compliance barriers that investors face when directly acquiring cryptocurrencies such as Bitcoin and Ethereum, including issues like private key management, taxation, fiat on-ramp/off-ramp, etc. These products have the potential to attract trillions of dollars into the cryptocurrency market.Compared to various existing products in the current financial market, why is the approval of a Bitcoin spot ETF by the U.S. SEC so crucial? There are two main reasons:

Access to a Larger Capital Base:

- Wide access to investors: A Bitcoin spot ETF can be listed on mainstream exchanges, reaching qualified investors, institutional investors, and retail investors at the same time. In contrast, trust structures like GBTC can only be traded on the OTC market and are limited to qualified investors. Moreover, US market is the largest market with best liquidity and greatest amount of capital in the world. Listing Bitcoin spot ETF in such huge market will attract more volume than any other market.

- Broader investment channels: traditional asset management sector, including fund managers and financial advisors, find it challenging to incorporate crypto assets into their portfolio without spot ETF.

Greater Acceptance:

- Bitcoin spot ETF products issued by institutions such as BlackRock and Fidelity are believed by many, more likely to be accepted by mainstream funds and investors due to the endorsement of these institutions' brands.

- Addresses compliance issues related to cryptocurrency assets; these products provide better clarity from compliance perspective, attracting more investment and contributing to the development of the related ecosystem.

As the largest capital market, the approval of a Bitcoin spot ETF in the United States would have a significant impact on the cryptocurrency market. These effects extend beyond increased inflow of funds to encompass the compliance of various participants in the global Bitcoin network and changes in Bitcoin network activities. We will continue to monitor the impact of these compliance measures on cryptocurrency assets and anticipate the shaping of a new generation of capital markets using public blockchain technologies.

Disclaimer:

This article and its contents are prepared solely for informational purposes only and do not replace independent professional judgement. Under no circumstances should the information contained herein be used or considered as an offer to sell, or solicitation of an offer to buy any security. The content of this presentation is proprietary and no part of it may be reproduced or redistributed without the prior written consent of DigiFT Tech (Singapore) Pte. Ltd. (Rreferred to as “the Company”). This article contains public information as of the specified date and may be stale thereafter. No representation or warranty, express or implied, is made as to the fairness, accuracy or completeness of the article and the information contained herein and no reliance should be placed on it. None of the Company, its advisers, connected persons or any other person accepts any liability whatsoever for any loss howsoever arising, directly or indirectly, from this article or its contents. All information, opinions and estimates contained herein are given as of the date hereof and are subject to change without notice. This material should not be viewed as advice or recommendations with respect to asset allocation or any particular investment.

比特币现货 ETF 临近,加密货币合规产品现状如何?

ETF 预期:加密市场的苏醒

随着加密货币十数年来一步步走入主流视野,从 Grayscale 的 GBTC 开始,传统市场的资金渠道流入情况越来越收到加密货币市场的关注。近期市场的回暖和传统机构有密切的关系:根据 CoinShares 的加密资产流动数据统计,从十月初开始,除了 12 月的一周有少量卖出之外,有连续十余周的净流入。比特币的价格也从 25000 美金左右的位置一路上涨超过 45000 美金。

市场普遍认为,这是投资者对美国 SEC 将会在一月份通过多家传统资管巨头比特币现货 ETF 的市场预期的体现。根据过往 ETF 审批流程来看,SEC 给出最终审批的时间最长为 240 天。Hashdex,Ark&21 shares 作为本批最早提交比特币现货 ETF 申请的机构,SEC 必须审批的截至时间点为 2024 年 1 月 10 日。如果这个比特币现货 ETF 被批准,那么大概率后续几家,如 BlackRock,Fidelity 等机构的比特币现货 ETF 大概率都会被批准。

而在美国比特币现货 ETF 被批准之前,资本市场早已经有合规的渠道获得加密资产敞口。早在 2013 年,灰度(Grayscale)的 GBTC 就已经上线,投资者能够通过传统券商渠道购买到 GBTC 信托的份额,从而间接持有比特币。

在过去的数年间,欧洲也有上百个和加密资产相关的 ETP 在传统交易市场上线,相关地区的投资人可以通过传统渠道购买到加密资产。大型资管巨头也有在非美国的资本市场发行比特币现货 ETF 产品,如 2021 年 Fidelity在加拿大多伦多股票交易所(TSX)上线和交易的比特币现货 ETF FBTC。

市场上已经不缺少购买到加密资产的渠道,那为什么大家如此关注美国比特币现货 ETF?这类产品和已有的合规加密资产购买渠道有何差异?

合规加密资产投资渠道现状

根据数字资产发行机构 CoinShares 每周统计全球各个地区合规加密资产产品的资金流动情况,数据包含各大机构发行的、投资于加密资产的、在传统金融渠道交易的产品,包括各类 ETP (Exchange Traded Products,交易所交易产品)和信托产品。该数据能够提现传统金融的资金,尤其是机构投资者资金对加密资产的投资资金进出情况,最新一期的数据截止于 2023 年 12 月 31日。

其中根据交易所在地区划分,各个地区的资管规模为:

这些渠道主要投资的资产为:

其中主要的资产提供方为:

其中,资管规模前五大的发行方情况和产品结构如下:

Grayscale Investments LLC

- 简介:Grayscale Investments 是全球领先的加密资产管理机构,总部位于美国。Grayscale 成立于 2013 年,是 Digital Currency Group 的子公司,并在 2013 年发行了比特币信托产品 GBTC。

- 主要产品:Grayscale Bitcoin Trust (GBTC)

- 法律结构:信托 (物理担保)

- 费用:2% 管理费

- 交易平台:OTCQX

- 发行日:2013.09.25 (inception date)

- 投资人要求:仅面向合格投资人和机构投资人

- 发行方加密资产总资管规模:33,370(单位:百万美元,2023.12.31)

CoinShares XBT

- 简介:CoinShares 是加密货币 ETP 行业的领先者,为投资者提供便捷、可靠的获取多样化的数字资产的交易所交易产品(ETP)。CoinShares 的 XBTProvider 是欧洲第一家为投资者提供轻松接触比特币和以太坊的合规产品的实体。

- 主要产品:Bitcoin Tracker One(COINXBT SS)

- 法律结构:跟踪证书(合成担保)

- 费用:2.5% 管理费

- 交易平台:纳斯达克斯德哥尔摩(Nasdaq Stockholm)

- 发行日:2015.05.18

- 投资人要求:北欧零售投资人

- 发行方加密资产总资管规模:2,374(单位:百万美元,2023.12.31)

21 Shares AG

- 简介:21Shares是全球最大的加密货币交易所交易产品(ETP)发行商,成立于 2018 年,总部位于瑞士苏黎世。其产品包括第一个物理担保的比特币和以太坊交易所交易产品(ETP)。

- 主要产品:21Shares Bitcoin ETP(ABTC)

- 法律结构:债务担保(物理担保)

- 费用:1.49% 管理费

- 交易平台:瑞士证券交易所

- 发行日:2019.2.25

- 投资人要求:北欧零售投资人

- 发行方加密资产总资管规模:2,336(单位:百万美元,2023.12.31)

ProShares ETFs

- 简介: ProShares是全球最大的 ETF 发行方之一,资管规模超过650亿美元。

- 主要产品:Bitcoin Strategy ETF(BITO)

- 法律结构:期货 ETF(合成担保)

- 费用:0.95%

- 交易平台:纽约证券交易所(NYSE)Arca

- 发行日:2021.10.18

- 投资人要求:美国零售投资人

- 发行方加密资产总资管规模:1,846(单位:百万美元,2023.12.31)

Purpose Investments Inc ETFs

- 简介:Purpose Investments是一家资产管理公司,管理着超过180亿美元的资产。Purpose Investments坚持不懈地专注于以客户为中心的创新,并提供一系列管理和量化投资产品。Purpose Investments由知名企业家Som Seif领导,是独立技术驱动型金融服务公司Purpose Financial的一个部门。

- 主要产品:Purpose Bitcoin ETF(BTCC)

- 法律结构:现货 ETF(物理担保)

- 费用:1.00%

- 交易平台:多伦多股票交易所(TSX)

- 发行日:2021.2.25

- 面向投资人:北美零售投资人

- 发行方加密资产总资管规模:1,764(单位:百万美元,2023.12.31)

和现货 ETF 相比,这些产品差异在哪里?

按照产品法律结构来划分,目前市场上合规加密货币产品可以分为 ETP(Exchange Traded Products)和信托(Trust)。其中 ETP 又可以进一步划分为 ETN(exchange traded notes,交易所交易票据),ETF(Exchange traded fund,交易所交易基金)和 ETC(Exchange traded commodities,交易所交易商品),其中加密资产相关产品以 ETF 和 ETN 为主。

其中,ETF 能够为投资者提供更好的可得性,能够同时投资于多种资产,费率更低、适合长期投资。但 ETF 容易出现跟踪误差,其 ETF 中的资产价值与其应跟踪的基准价值之间存在差异,最终可能导致回报低于预期的情况出现。此外,ETF 在税务,申购赎回流程,流动性等问题上有更高的复杂度。

ETN 是一种债务结构,一般是由金融机构发行的无担保债务工具,投资者购买的是发行方的债务,通常由于信用问题因此对投资者有更高的风险。相比于 ETF 结构,一般来说 ETN 的流动性会更差。但 ETN 的好处在于,能够提供更多样化的资产类型,不会有跟踪误差的问题,税务上也能更加灵活。在上述几个产品中,21Shares Bitcoin ETP 就是典型的 ETN 产品。

信托结构相对比较复杂,一般只能在 OTC 市场进行交易,如 Grayscale 的 GBTC 仅在 OTCQX 上交易,这类平台流动性较差、投资者数量较少,OTCQX 整个平台日交易量也仅达到 13 亿美元(2024.01.02) 。此外,Grayscale GBTC 通过信托结构发行,只能单向申购,无法赎回;投资者在申购后六个月才能获得发行的份额并在二级市场交易,这样的性质是导致 GBTC 在牛市产生正溢价,在行情低迷时产生负溢价的原因。

进一步,上述产品若根据底层资产划分,可以分为两类:物理担保(Physically backed)和合成担保(Synthetically backed)。

物理担保 ETP:购买实物底层资产并持有,从而产品份额的价格能够跟踪底层资产的价格。物理担保的产品表现和相关资产的表现直接相关。如 Purpose Investment 的 BTCC,是在多伦多股票交易所上线的现货 ETF,每一份 ETF 都对应一定数量的、直接由 ETF 管理方持有的比特币,一般比特币会有专业的托管机构持有,如BTCC托管方为 Gemini Trust Company 和 Coinbase Trust Company。

合成担保 ETP:使用与交易对手(通常是银行)的互换协议来提供标的资产的回报。为确保每天交付回报,掉期交易对手通常需要向发行人存入由独立托管人持有的抵押品(通常为国债或蓝筹股)。所需的抵押品金额随跟踪的资产价值而波动。如 ProShares BITO,是在纽约证券交易所的比特币期货 ETF,基金投资于CME 上的比特币期货。

SEC 通过比特币现货 ETF,会有怎么样的市场影响?

上述各类在传统金融渠道交易的加密货币金融产品为投资者提供了一站式获得加密资产敞口的渠道,绕开了困扰投资者直接获取比特币、以太坊等加密货币的各类技术、合规的门槛,如私钥管理、税务、法币出入金等,从而吸引数万亿美金的资金进入加密货币市场。

和当前金融市场上已有的各类产品相比,美国 SEC 批准的比特币现货 ETF 为什么那么重要?主要有两个原因:

触达更大的资金面:

- 更多的投资者。美国是最大的金融市场之一,比特币现货 ETF 上架在主流交易所,能够同时触达合格投资者、机构投资者和零售投资者。而 GBTC 等信托结构的产品只能在 OTC 市场供合格投资者交易,同类的比特币现货 ETF 产品在欧洲、加拿大等地区的交易所交易,相比美国市场,流动性更差,资金体量更小。

- 更广阔的投资渠道。传统资产管理部门,如各类基金经理、财务顾问等在没有比特币现货 ETF 的情况下很难将加密资产纳入他们的投资组合中。

更好的接受度:

- 由 Blackrock,Fidelity 等机构发行的比特币现货 ETF 产品,会由于这些机构的品牌背书更容易被主流资金接受

- 解决了加密资产的合规问题;这类产品会有更高的合规清晰度,吸引更多的投资和相关生态的建设

美国作为最大的资本市场,若比特币现货 ETF 得到通过,将会为加密资产市场带来巨大的影响,这些影响不仅仅是更广阔的资金来源流入,还会关系到全球各个比特币网络相关参与方的合规化,以及对比特币网络活动的变化。我们会持续观察这些资产合规化对加密资产的影响,期待加密资产塑造新一代的资本市场。

免责声明

本文及其内容仅供信息目的使用,不替代独立的专业判断。在任何情况下,本文所包含的信息不应被视为出售或购买任何证券的要约或征求。未经DigiFT Tech (Singapore) Pte. Ltd.(称为“公司”)事先书面同意,任何部分均不得复制或重新分发。本文包含的公开信息仅截至指定日期,并可能在此后过时。对于文中和其中所包含的信息的公正性、准确性或完整性,不作任何明示或暗示的陈述或保证,不应依赖于此。公司、其顾问、关联人员或任何其他人对于由于本文或其内容而直接或间接引起的任何损失概不承担任何责任。本文中所包含的所有信息、观点和估计均截至本日期,并且可能随时变动,恕不另行通知。本材料不应被视为关于资产配置或任何特定投资的建议或推荐。